Introduction

Today’s market is globalized; business is taking societal and environmental responsibility, and business is focusing on corporate social responsibility (CSR) to contribute to societal well-being and also make sure that they have sustained growth in the competitive market. CSR includes a broad range of activity, from sustainable environment to community engagement and managing the ethical labor practices. For stakeholders ranging from customers to investors, it’s a place for growing corporate responsibility for the society; the blending between CSR and business strategy has changed from optimal to critical. The game between CSR and profitability has been an extensive research focus and debate (1). The CSR is imposing additional costs on the organization; their profitability is reducing, but in another way the CSR can give a sustainable economic gain by giving them an opportunity for brand reputation, customer loyalty, and improving operational efficiencies. The main challenge is balancing between the short-term costs of CSR and the long-term benefits it can provide.

In 2022, amended by the company’s amendment rules, 2014 (CSR policy), under this section 135 and subsection (1) and (2) of the Companies Act, 2013, section 469, CSR amendments introduce specified requirements for the calculation of costs associated with the social impact assessments and managing unspent funds of CSR, and upcoming CSR activity is institutionalized in the corporate framework.

This type of analysis helps to interplay between CSR and the profitability of an organization to achieve both financial growth and a positive impact on the social impact. By analyzing literature, case studies, and implications of the 2022 amendments, this CSR study is designed to get an understanding of the CSR activity and how it’s driving the company’s sustainable long-term growth and profitability.

Literature review

Mishra and Suar (2) demonstrated that industries such as Fast-Moving Consumer Goods (FMCG) and pharmaceuticals benefit more from CSR due to direct consumer interaction, leading to enhanced brand loyalty. On the other hand, capital-intensive industries like oil and gas and automotive faced challenges in converting CSR spending into direct financial gains due to high operational costs and market volatility.

Carroll and Shabana (3) assert that CSR contributes to long-term financial performance by enhancing brand reputation, increasing customer loyalty, and improving employee engagement. Similarly, we can see that Porter and Kramer (4) introduce the concept of creating shared value (CSV), arguing that CSR is not merely a philanthropic activity but a strategic tool for achieving competitive advantage. These foundational theories suggest that when CSR initiatives align with corporate goals, they can drive profitability rather than merely serve as additional costs.

Bhunia and Das (5) analyzed Maharathna companies in India and found a mixed impact of CSR on profitability, indicating that industry-specific factors play a crucial role. Their findings showed that while CSR had an inverse relationship with profit after tax in companies like BHEL and ONGC, it had a positive impact on firms like GAIL and NTPC. This suggests that the financial benefits of CSR are contingent on how well the initiatives align with a firm’s operational strategy.

Rathod (6) did a study on the Indian banks and found that the CSR spending positively affected financial health, particularly in terms of return on assets (ROA) and net interest margin (NIM). This study concluded that CSR enhances customer trust and regulatory compliance, leading to sustained profitability in regulated industries like the banking and finance sectors.

Sawant (7) examined the manufacturing firms and highlighted that a firm with well-integrated CSR strategies experienced higher financial returns due to improved customers, suppliers, investors, and employee relationships and operational efficiency. The study emphasized the role of regulatory policies in ensuring the CSR’s effectiveness.

KPMG (8) suggests that technology firms like Infosys and TCS have successfully leveraged CSR to enhance innovation and brand perception, translating into long-term profitability. The study noted that in technology-driven industries, CSR initiatives related to digital inclusion, education, and sustainability are particularly effective in improving financial outcomes.

Scope of study

This study is focusing on the role of CSR in the financial growth of publicly listed companies in India. The data for the study covers a 10-year period from 2013 to 2023. Our aim is to analyze CSR spending on CSR activity. Is it worth it or not for an organization? We are taking indicators like ROA, ROE, and net profit. Our study aims to provide insights on whether the CSR activity can really give an opportunity to build strong financial growth or not and how they can use the CSR activity to their brand reputation and build sustainable growth in the competitive market.

Study design

This study follows a quantitative approach, utilizing descriptive and inferential statistical methods to know the relationship between the CSR expenditure and financial performance. This study employs a panel data analysis, allowing for a detailed examination of firm-level trends over time. By incorporating multiple regression analysis, correlation analysis, and hypothesis testing, this study aims to determine the extent to which CSR spending translates into financial gains and sustainable business growth.

Objectives of the study

To analyze the relationship between CSR expenditure and financial performance indicators (ROA, ROE, and net profit margin) among the Indian industry and firms.

To examine the sector-specific variations in the impact of CSR spending on financial performance in the competitive market.

To evaluate the influence of regulatory amendments, particularly the Companies (Amendment) Act, 2022, on CSR implementation and corporate profitability.

To provide strategic recommendations for companies to optimize CSR investments for sustainable financial performance.

Data collection

Annual reports of selected companies, including financial statements and CSR disclosures.

CSR disclosures mandated under section 135 of the Companies Act, 2013, and its subsequent amendments.

Regulatory filings from the Ministry of Corporate Affairs (MCA) of India and stock exchanges (NSE/BSE).

Sampling unit

The selection of companies for this study draws upon the top 1,000 rankings from the Economic Times and Business Today reports covering 2015 through 2022. The technology company and manufacturing companies are designated as sample units for this study. We have chosen the company based on some factors like market cap, net profit, total assets.

Sampling size

Indian top manufacturing and technology’s 40 companies

Sampling method

For the sampling method, the stratified method is used. At the first step, all the manufacturing and technology companies are systematically divided into eight categories, namely technology, cement, pharmaceutical, auto, oil and gas, FMCG, chemical and mining and fertilizers. During the second step, we choose five companies form each sector for the research, culminating in a total of 40 companies under study.

Data analysis techniques

Correlation analysis—to assess the relationship between CSR expenditure and profitability indicators (ROA, ROE, and net profit margin).

Hypothesis testing—using a t-test to evaluate the statistical significance of CSR’s effect on profitability.

Sector Comparison—examining how the different industries respond to CSR investments in terms of financial returns and sustainability.

Regulatory context

This study integrates key regulatory changes brought by the companies Amendment Act, 2022, which was introduced.

Mandatory disclosure of unspent CSR funds and their reallocations.

Stricter impact assessment mechanisms to measure CSR effectiveness.

Revised compliance guidelines and penalties for non-compliances.

Limitations of the study

Industry-specific bias

The study is limited to manufacturing and technology sectors, potentially limiting applicability to the other industries.

Limited sample size

This analysis is based on the 40 companies, which may not fully capture broader trends in the Indian corporate landscape.

External market factors

Variables such as inflation, taxation policies, economic downturns, and market volatility may influence profitability beyond the CSR investments (Table 1).

Table 1. List companies under study.

Net profit margin

The net profit margin is valuable when we are calculating for the purpose of overall profitability of the business and to know the efficiency of the business operations. This ratio is necessary to articulate the cost of efficiency in the operation. If a business is making a high net profit margin, we can say that the business is making sufficient returns for the owner and positions the business to withstand economic downturn conditions.

Profit after tax

Formula

Actual CSR expenditure percentage on current year’s net profit.

Hypothesis

H0: If the current year profit significantly equals our standard expected expenditure (2%) as per norms, then the distribution of actual percentage expenditure on CSR, then H0 is accepted.

H1: If the current year profit is significantly not equal to our expected expenditure (2%) as per norms, then the distribution of the actual percentage expenditure on CSR is H1 accepted.

H0: The statistical relationship between the profitability in the subsequent years and CSR spending in the prior years across the chosen industries

H1: There is no statistically significant correlation between the previous year’s CSR expenditure and subsequent profit in the chosen industries (Tables 2, 3).

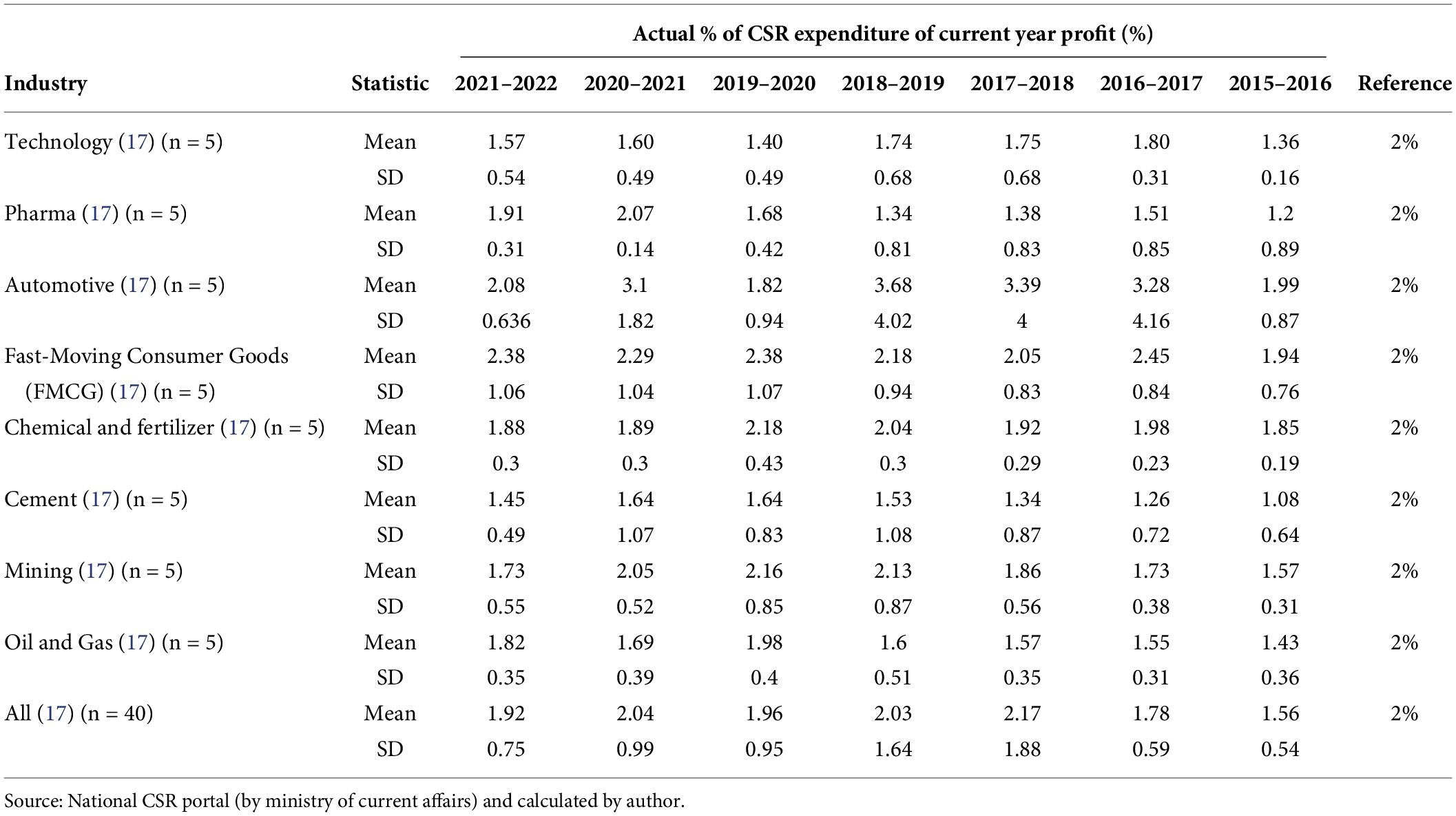

Table 2. The average distribution (mean) of actual corporate social responsibility (CSR) expenditure percentage in relation to each financial year and industry type of current year’s profit.

Table 3. Statistical average of the comparison (mean) of the actual percentage of CSR expenditure of the current year’s profit against the value of reference (2%) for the first four industry sectors and respective years across.

Given that the reference p-value obtained from the one-sample t-test is 2.0%, which is less than the significance threshold of 0.05, the null hypothesis (H0) is rejected, indicating a statistically significant difference. Consequently, we accept the alternative hypothesis (H1). Conversely, if the p-value was greater than 0.05, we would fail to reject the null hypothesis (H0) and reject the alternative hypothesis (H1). In the present analysis, however, the null hypothesis (H0) is retained, and the alternative hypothesis (H1) is rejected (Table 4).

Table 4. Average statistical average comparison (mean) of the actual % of the CSR activity expenditure of the present year profit with reference value (2%) in the industry type and respective financial years (next four and overall).

Here, we have a reference value sample t-test with a p-value = 2.0% (H0) null hypothesis. We are rejecting and accepting the (H1) alternative hypothesis if the p-value is less than 0.05; if not, then the null hypothesis (H0) is going to be accepted and (H1) is going to be rejected.

The CSR average expenditure as a percentage of present-year profit is significantly different from the reference value of 2.0% across all financial years, with p-values less than 0.001. Until 2016–2017, the expenditure was notably lower than 2.0%, but from 2017 to 2018 onward, it exceeded 2.0%. Notably, industries like cement, iron, steel, and mining have been closer to the 2.0% target post-2018–2019, while sectors like pharma, chemical, technology, and oil and gas have consistently deviated from the benchmark throughout the study period from 2015–2016 to 2021–2022.

Corporate social responsibility % and net profit margin %

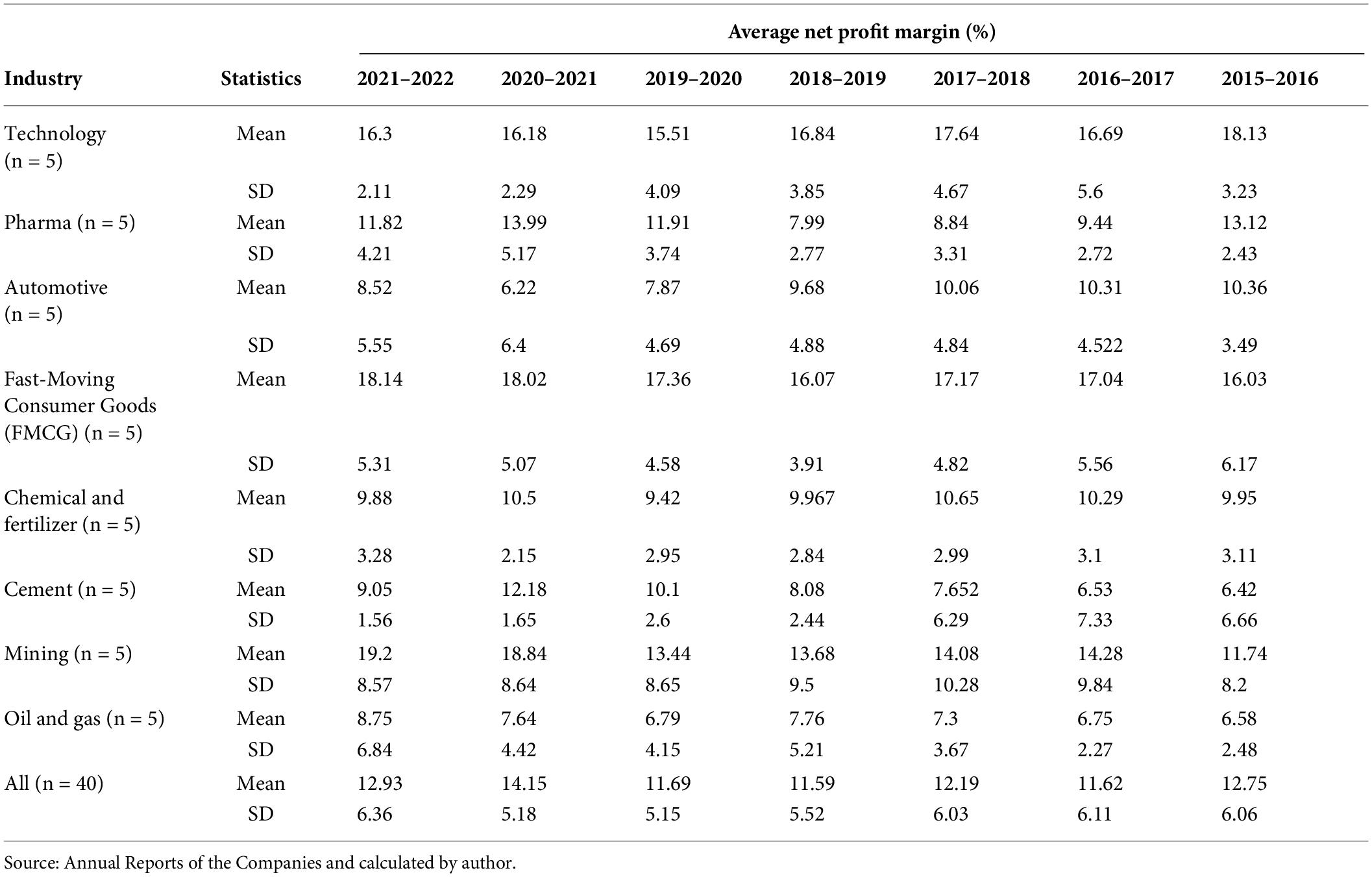

Tables 5 and 6 show that the mining industry consistently has the highest average % net profit margin across financial years, followed by the FMCG and pharma industries. In contrast, the automobile and oil and gas industries have lower average % net profit margins. Overall, the % net profit is relatively stable across all industries and financial years (Table 7).

Table 5. Average distribution (mean) actual % of expenditure of present year net profit in the respective financial years and industry type.

Table 6. Average net profit margin distribution (%) by financial year and type of industry.

Table 7. The correlation within the CSR expenditure and across the financial year’s net profit margin and the sector study.

The percentage of CSR expenditure is positively and significantly linked to the net profit margin of upcoming years across all kinds of industries researched. p-value less than 0.05. We are going to reject H0 and hence accepte H1.

Findings

The study reveals a significant positive connection between the CSR expenditure and net profit margins across various industries from 2015–2016 to 2021–2022. This trend suggests that firms with higher CSR investments generally experience increased profitability in subsequent years. This finding reinforces previous literature, which concludes that we have to look at CSR as an investment rather than a cost.

Sector-wise analysis

Mining and FMCG industries

The mining industry consistently makes the highest average net profit margins, reaching 19.2% in 2021–2022. This gives knowledge about how CSR initiatives in the sector have played a crucial role in enhancing customers, investors, employees, suppliers, the government’s trust, and operational efficiency.

Similar to that, the FMCG companies demonstrated stable profitability, reinforcing the idea that CSR enhances brand loyalty and customer trust gained. These findings are aligned with Mishra and Sura (2), who found that CSR significantly influences firm performance in consumer-driven industries.

Technology sector

Firms like TCS and Infosys demonstrated strong financial performance during 2021–2022, with an average net profit margin of 16.3%. This indicates the technology firm’s efficiency in leverage CSR to enhance brand reputation and risk in the competitive market, ultimately contributing to sustained financial success. The findings are consistent with Sawant (7), who highlighted that CSR in technology-driven firms leads to long-term profitability and market stability.

Pharmaceuticals industry

The pharmaceutical sector displayed variable net profit margins, with a peak of 13.99% in 2020–2021. This variation is attributed to factors such as high-margin patented products and market demand fluctuation. Companies like Cipla and Sun Pharmaceutical successfully balanced CSR activities with competitive pressures, supporting Rathod (6), who found that engagement strengthens financial health in the regulated firms and industries like banking and pharmaceuticals.

Automotive and oil and gas sectors

The automation sector—when we focused on that we came to see that the average net profit margin was 8.52% in the year 2021–2022, while the oil and gas sector recorded 8.75%. These industries have maintained stable profit margins through activity. But the lower profitability compared to other sectors reflects the financial challenges in these firms and industries. These results partially support Bhunia and Das (5); he found that the connection between CSR and profitability varies significantly across firms and industries.

Chemical and fertilizer industry

When we are looking at the chemical and fertilizer sector, it reported the lowest average net profit margin (9.88% in 2021–2022). This is attributed to price volatility and regulatory challenges, which limit the financial benefits of CSR investments in this sector. The finding aligns with prior research that highlights industry-specific constraints in realizing CSR’s full potential.

Statistical validation

The study’s hypothesis testing confirms that the percentage of CSR expenditure is positively and significantly correlated with the net profit margins across all the firms and industries, with the p-values consistently below 0.05.

The mining, FMCG, and technology sectors exhibited the strongest correlation between the CSR activity, leading to the rejection of H0 in multiple financial years.

The automotive and cement industries showed mixed results, where actually CSR expenditure remained below the expected 2% benchmark for most years, confirming the findings of Bhunia and Das (5) that some industries face financial constraints in CSR investments in the competitive market.

Conclusion

This study underscores the strategic importance of CSR activities, particularly in industries like mining, FMCG, and technology, where CSR investments have resulted in tangible financial gains. The findings reinforce that the CSR is not just a regulatory obligation but a strategic tool for building brand reputation and employees’, customer’s, suppliers’, investor’s, and government’s trusts, and balanced profitability. Moving forward, companies should integrate CSR more effectively with their corporate strategies to maximize financial and social benefits.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

1. Margolis JD, Elfenbein HA, Walsh JP. Does it pay to be good? A meta-analysis and redirection of research on the relationship between corporate social and financial performance. Acad Manag Perspect. (2009) 23(3):5–18.

2. Mishra S, Suar D. Does corporate social responsibility influence firm performance of Indian companies? J Bus Ethics. (2010). 95(4): 571–601.

3. Carroll AB, Shabana KM. The business case for corporate social responsibility: a review of concepts, research and practice. Int J Manag Rev. (2010) 12(1):85–105.

5. Bhunia A, Das L. Corporate social responsibility and profitability: a study of Maharatna companies in India. Int J Bus Ethics. (2015) 10(2):112–25.

6. Rathod P. Impact of CSR activities on the financial performance of Indian Banks. J Manag Res Anal. (2016) 3(1):14–20.

7. Sawant PD. The impact of corporate social responsibility on profitability of companies: a study on select manufacturing companies in India. Econspeak J Adv Manag IT Soc Sci. (2018) 8(5):5–12.

8. KPMG. The Future of Corporate Social Responsibility: Global Trends and Challenges. KPMG Sustainability Report (2020).

9. Companiesmarketcap. (n.d.). Available online at: https://companiesmarketcap.com/india/largest-companies-in-india-by-market-cap/

10. Appreciate. (n.d.). Available online at: https://appreciatewealth.com/blog/best-chemical-stocks-in-india

11. Onsite. (n.d.). Available online at: https://onsiteteams.com/best-cement-in-india-types-of-cement-latest-rates/

12. WeblineIndia. (n.d.). Available online at: https://www.weblineindia.com/blog/top-25-it-companies-in-india/

13. GlobalData. (n.d.). Available online at: https://www.globaldata.com/companies/top-companies-by-sector/healthcare/india-companies-by-market-cap/

14. Tickertape. (n.d.). Available online at: https://www.tickertape.in/stocks/collections/fmcg-stocks

15. Appreciate. (n.d.). Available online at: https://appreciatewealth.com/blog/oil-and-gas-stocks-in-india

16. Indiancompanies.in. (n.d.). Available online at:https://indiancompanies.in/top-companies-in-steel-industry-in-indiaby-capacity-market-share/

17. The CSR Journal. (n.d.). Available online at: https://thecsrjournal.in/top-companies-india-csr-sustainability-2022/

© The Author(s). 2025 Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.