Introduction

The swift onset of internet technology has provided numerous types of facilities in numerous employments, one of which is buying and selling transactions. Many business organizations around the world aspire to become major hubs of international trade through significant investment and contributions in e-commerce and global IT industries. Internet evolution has a notable impact in numerous forms, banking sector is mostly updated by IT. The latest service of banking is Internet banking. The banking transaction through internet banking is very swift and prompt, simple, secure and the lowest level price can be assisted by electronic trade. Internet banking can help customers to complete various payment quickly and correctly without going to bank premises.

In this research the author used Technology Acceptance Model (TAM) which is a well approved model to analysis how technology adoption change manual banking to internet based banking

Hence, internet banking highly upgrade the payments and receipts in e-commerce related deal and settlement. This research showed that how internet banking of Islami Bank Bangladesh PLC can have a factual impact on e-commerce build out in Bangladesh.

In this research, the author also focused on function and scope of Internet banking service of Islami Bank Bangladesh Limited (IBBL), E-commerce of Bangladesh, this research describe the mobilization of e-money to expedite dealings by web based commerce or digital commerce. The research was performed to find out the significance of Internet banking service of IBBL with E-Commerce traders of Bangladesh.

Research questions

1. To what extent Islami Bank Bangladesh Ltd made it easy to handle customer’s issue in performing E-Commerce related transaction?

2. To what extent Islami Bank Bangladesh Ltd accelerate the E-Commerce related transaction through Internet Banking service?

3. To what extent and how Islami Bank Bangladesh Ltd help to improve E-Commerce related transaction through Internet Banking service?

4. What are the differences in customer attitudes towards internet banking between IBBL and Sonali Bank Plc?

Objectives of the research

General objective: To assess the impact of Internet banking of E-Commerce upon the customers of IBBL.

Specific objectives: The author define some specific objective of the research which are given below:

1. Expand the scope of E-Commerce and Internet banking in all branch of IBBL.

2. Ensure all customers are getting the facilities of Internet banking to perform E-Commerce related transaction and others.

3. Make ease the function of Internet banking on E-Commerce related transactions.

4. Evaluate the customers satisfaction using Internet banking of IBBL to perform E-Commerce related transactions.

Scope of the research

E-commerce, or electronic commerce, refers to the buying and selling of goods and services over the internet. It encompasses all online transactions, from browsing a website to delivery of a purchase. Essentially, it’s the practice of conducting business through the internet.

Internet banking and e-commerce are intertwined and crucial for modern financial transactions. Internet banking provides the infrastructure and security for e-commerce, enabling online payments and financial transactions. E-commerce, in turn, leverages internet banking to facilitate the buying and selling of goods and services online.

As a fast-growing sector with an ever-expanding requirement of employees, Banking attracts customers hailing from various professional specializations, especially the commerce field.. In this study the author focus the largest bank of Bangladesh, its Internet banking service and E-Commerce business as a whole.

Limitations of the research

1. The sample size is too large to examine.

2. It is too hard to establish such a server to bring all the customer of IBBL under Internet banking and E-Commerce services.

3. Its required much time to study the whole population.

4. Sometimes all data and information could not be acquired properly and timely.

Literature review

Modern banking and e-commerce are deeply intertwined, with e-commerce greatly benefiting from the advancements in electronic banking services. These services, including online banking, mobile banking, and payment gateways, have enabled seamless transactions and financial operations for e-commerce businesses.

Internet banking, also known as online banking, is a service that allows us to conduct financial transactions and manage our bank account remotely through a secure website or mobile app. It provides access to features like checking balances, transferring funds, paying bills, and accessing statements.

E-commerce and payment systems work hand-in-hand, facilitating the buying and selling of goods and services online. E-commerce refers to the transaction of goods and services over electronic networks like the internet. Payment systems, in turn, are the digital infrastructure that allows for the secure and convenient transfer of funds between consumers and merchants.

Background of the organization

Islami Bank Bangladesh Limited (IBBL) is a top ranked bank in Bangladesh providimg devoted service to its customers. This bank launch many services, make existing services faster and better than ever. Now this bank launched Internet banking service to provide their customers more facilities.

Islami Bank Bangladesh Ltd (IBBL), established in 1983, is the first Shariah-based Islamic bank in South-East Asia. It’s a joint venture, public limited company with foreign institutions as majority shareholders, listed on both Dhaka and Chattogram stock exchanges. IBBL is known for its extensive branch network, general banking services, commercial investment, and foreign exchange activities, as well as its role in Islamic microfinance.

E-commerce & modern banking

Electronic commerce (e-commerce) and modern banking are closely interlinked, with e-commerce relying heavily on banking systems for payment processing and transactions. Modern banking has evolved to support e-commerce through online banking platforms, mobile banking apps, and various digital payment methods. This integration has led to significant changes in how businesses and individuals conduct transactions and manage their finances.

E-commerce and modern banking are increasingly intertwined, with banks playing a crucial role in enabling online transactions and providing digital payment solutions. This integration has brought numerous benefits, but also presents challenges related to security, regulation, and technological infrastructure. As technology continues to evolve, the relationship between e-commerce and modern banking will continue to evolve, shaping the future of financial transactions and commerce.

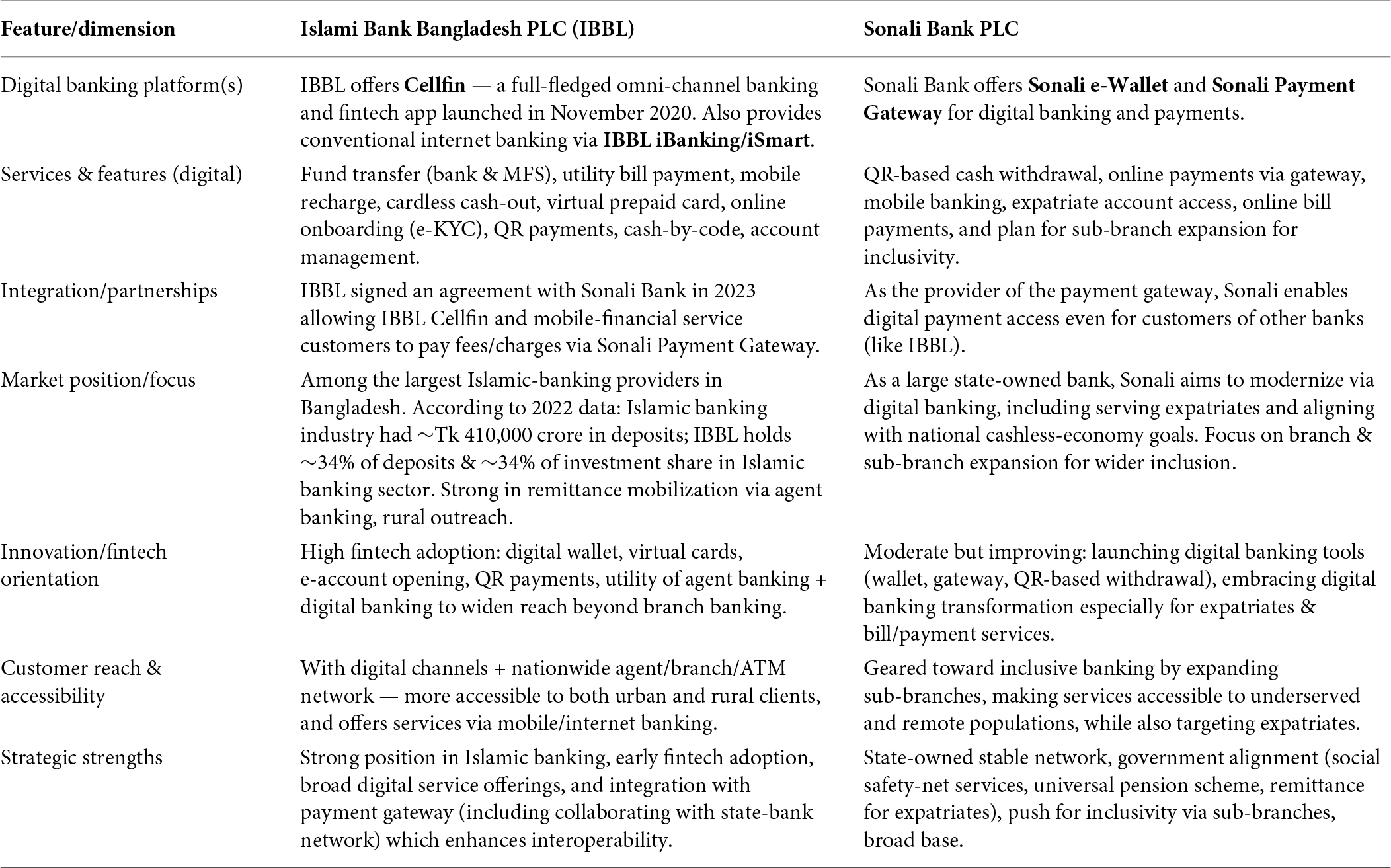

Table 1. Comparison between Islami Bank Bangladesh Ltd and Sonali Bank PLC in terms of net banking.

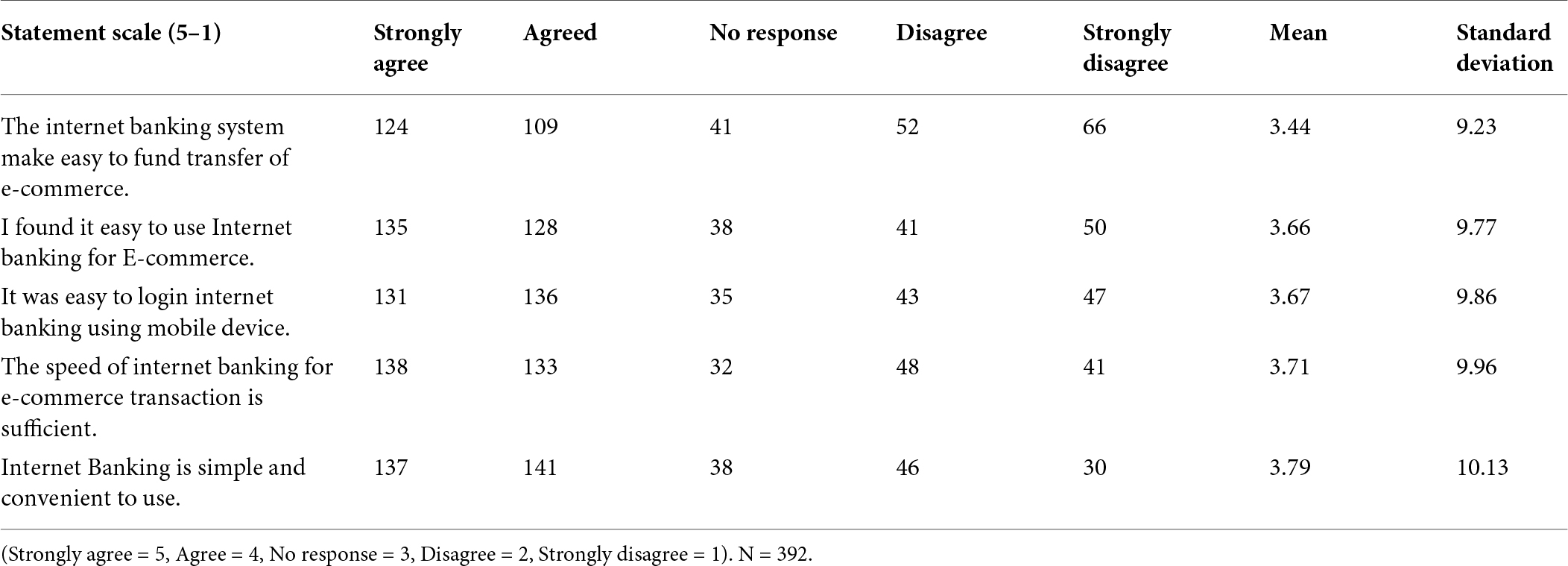

Table 2. Ease of use of internet banking in e-commerce transaction.

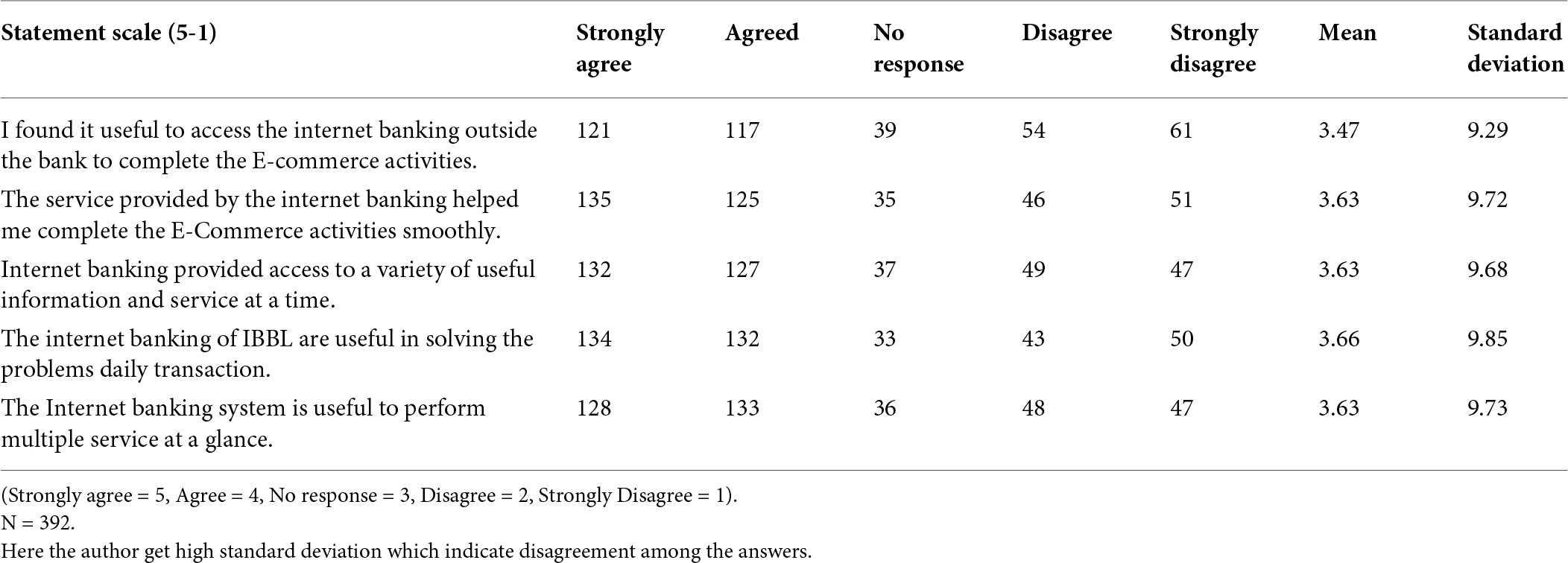

Table 3. Perceived usefulness internet banking in e-commerce transaction.

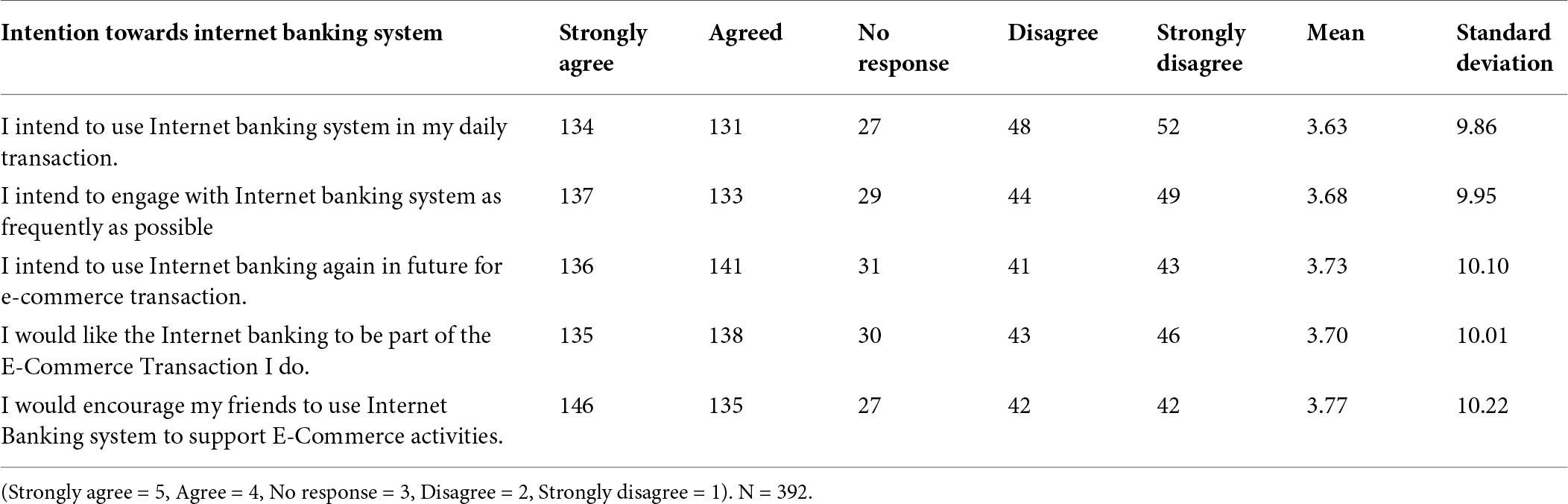

Table 4. Intention to use internet banking in e-commerce.

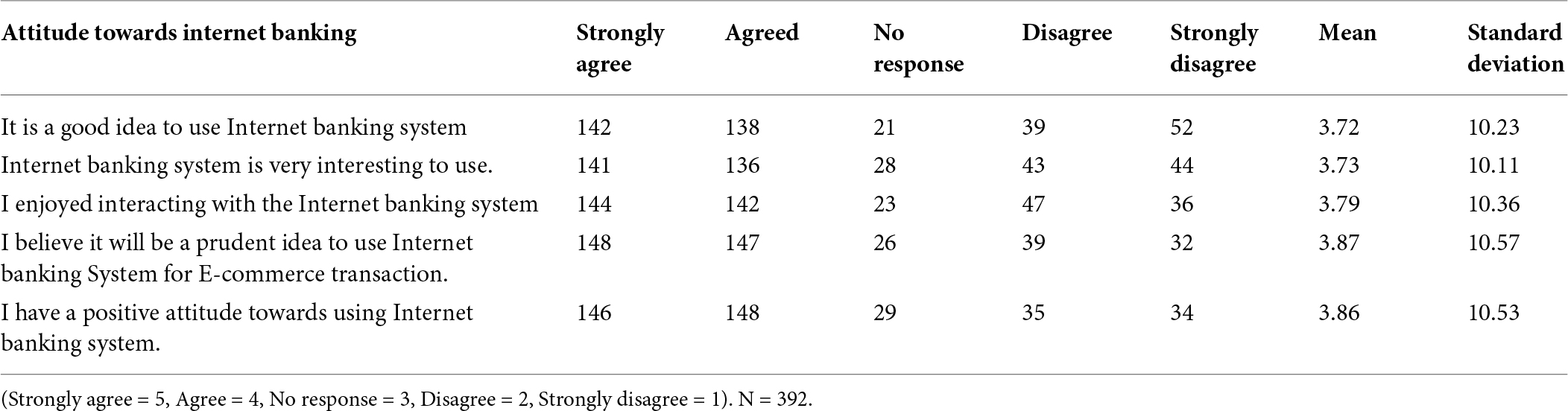

Table 5. Attitude towards using internet banking in e-commerce transaction.

Applications of banking service in e-commerce

Some of the most important current application of e-commerce in banking.

1. Electronic billing system

2. ID verification tool,

3. Mobile payments system.

4. Digital-only banking service,

5. B2B innovation method.

6. International commerce.

E-commerce relies on secure online payment processing, which is facilitated by banks and payment gateways. Banks provide the infrastructure for verifying transactions, handling credit card payments, and ensuring the security of online purchases.

Modern banking offers various digital payment methods, such as mobile wallets, online transfers, and digital currencies, which are widely used in e-commerce. Banks have developed online banking platforms that allow customers to manage their accounts, make transfers, and track their transactions, all from the comfort of their homes.

Mobile banking apps provide users with convenient access to their bank accounts and various banking services, including online payments and fund transfers, which are crucial for e-commerce transactions.

Banks implement robust security measures to protect e-commerce transactions from fraud and cyber threats, ensuring a safe and secure online shopping experience. E-commerce has spurred innovation in banking, leading to the development of new products and services, such as mobile payments, online loan applications, and digital investment platforms.

Table 6. Association between PEU & attitude.

Table 7. Regression analysis of PEU & attitude.

Internet banking service of IBBL

Online banking, also known as internet banking, virtual banking, web banking or home banking, is a system that enables customers of a bank or other financial institution to conduct a range of financial transaction through the financial institution’s website or mobile app.

Today Internet banking service of Islami Bank Bangladesh Lid is popular. To operate internet banking service an account holder need a valid email address and smart phone or laptop/PC.

Internet banking, also known as online or digital banking, allows you to conduct financial transactions securely through a bank’s website or mobile app, offering convenience and access to our accounts anytime, anywhere.

Internet banking is a service provided by financial institutions that allows customers to access and manage their accounts, perform transactions (like transfers, bill payments, and balance inquiries), and access other banking services remotely via the internet.

How it works

We access our bank’s online banking platform through a secure website or mobile app, using our registered username and password.

Benefits

Convenience: You can manage your finances from anywhere with an internet connection, 24/7.

Time-saving: Avoid trips to the bank and long queues.

Security: Banks use encryption and other security measures to protect your data and transactions.

Access to a wide range of services: You can perform various banking activities online, including checking balances, transferring funds, paying bills, and more.

Table 8. Association between PU & attitude.

Table 9. Regression analysis of PU & attitude.

Examples of internet banking services

Account Management: Checking account balances, transaction history, and statements.

Fund Transfers: Transferring money between your own accounts or to other accounts.

Bill Payments: Paying bills online.

Loan Management: Viewing loan details, making payments, and applying for loans.

Credit Card Management: Managing credit card transactions, payments, and limits.

Security measures

Strong Passwords: Use strong, unique passwords and change them regularly.

Two-Factor Authentication (2FA): Some banks offer 2FA, which requires an additional verification step (like a code sent to our phone) in addition to our username and password.

Secure Websites: Ensure we are accessing the bank’s official website and not a phishing site.

Regularly Check Transactions: Monitor our account activity regularly to detect any unauthorized transaction

Advantages of internet banking

Given below are some advantages/benefits of Internet Banking available for all the users-

1. 24 × 7 hours availability.

2. Convenience of initiating financial transactions

3. Proper Track of any transactions,

4. Quick and Secure payment system.

5. Non-financial Transactions.

There are three types of fund transfers which can be made using net-banking such as national electronic fund transfer (NEFT), real-time gross settlement (RTGS), national payment switch board (NPSB).

Table 10. Association between attitude & intention.

Table 11. Regression analysis of attitude & intention.

Comparison between customer attitudes towards internet banking between Islami Bank Bangladesh Limited and Sonali Bank Plc

Sonali bank is a state owned bank of Bangladesh. It also offer internet banking service to its customers. Sonali Bank’s internet banking service has some specific features such as fund transfers (BEFTN), utility/govt. bill payments (NBR customs, taxes), mobile top-ups, account management (balance/statements), and corporate services with multi-tier approvals, integrated with government platforms for seamless digital payments, all accessible via web and mobile apps like Sonali eSheba and e-Wallet for convenience and digital transformation.

While Islami Bank Bangladesh Ltd. (IBBL) is a major private bank known for its digital focus, and Sonali Bank is a large state-owned bank, determining which “internet banking” is more active depends on user experience (UX), features, and recent upgrades. IBBL often leads in private digital banking, while Sonali offers broad reach but has faced challenges in tech modernization, though both offer mobile/online banking, with IBBL generally seen as more tech-savvy for retail users.

Table 12. Age & intention to use.

Key differences & activity

• IBBL (Islami Bank): A large private bank, often praised for its extensive digital offerings (apps, cards, Shariah-compliant services), making it very active for tech-savvy customers.

• Sonali Bank: The nation’s largest state-owned bank, providing wide access, but historically slower in adopting cutting-edge digital tech compared to private players, though they are upgrading.

• Activity: IBBL’s digital platforms (like mCash) are highly used for daily transactions, while Sonali’s strength lies in its vast network and government services, with growing digital adoption.

From the above mentioned discussion the author can conclude that,

• Features: IBBL offers more modern, integrated Islamic digital banking.

• Reach: Sonali has branches everywhere, but its i-banking might feel less fluid.

• User Reviews: Search recent reviews for “IBBL app” vs. “Sonali Bank iBanking” for current user sentiment on performance and stability.

In essence, IBBL is often considered more digitally innovative, while Sonali Bank provides essential scale and reach, making digital activity a matter of user priority and specific need

Brief introduction of TAM model

The TAM is a theory that explains how users come to accept and use new technology, focusing on two key factors: perceived usefulness and perceived ease of use. TAM is a behavioral/cognitive psychology model that helps understand why people adopt or resist new technologies. The model was developed by Fred Davis and Richard Begoni in 1989.

Key factors

Perceived Usefulness: The extent to which a user believes that using a particular technology will help them perform their tasks better or achieve their goals.

Perceived Ease of Use: The extent to which a user believes that using a particular technology will be effortless and straightforward.

How it works

TAM posits that these two perceptions (perceived usefulness and perceived ease of use) directly influence a user’s attitude towards using the technology, which in turn affects their intention to use it, ultimately leading to actual usage behavior.

Applications

Technology Acceptance Model (TAM) has been used in various contexts, including research on the acceptance of new e-technology or e-services, and is a widely applied model of user acceptance and usage.

TAM, UTAUT, internet banking & e-commerce

The method used was the quantitative research method. In this research the author conduct face to face interview and inspect the impact of internet banking of e-commerce related transaction. The author determined how much influence internet banking of IBBL has on e-commerce (1).

Table 13. Demographic (age) data of customers of IBBL.

Table 14. One-way anova test between the level of computer skill and customer’s intention to use internet banking.

Technology Acceptance Model (TAM) was first introduced by Davis in 1986. The TAM is a theory that explains how individuals accept and use new technology. It’s based on the idea that users are more likely to adopt technology if they perceive it as useful and easy to use. The model is widely used in information systems and other fields to predict the likelihood of technology adoption (2).

The TAM is an information systems theory that models how users come to accept and use a technology. The actual system use is the end-point where people use the technology. Behavioral intention is a factor that leads people to use the technology [Foon et al. (3) Internet banking adoption in Kuala Lumpur: an application of unified technology acceptance and use of technology theory (UTAUT) model.]

The UTAUT (4). UTAUT comprises of four main factors. These are; performance expectancy, social influence, effort expectancy and facilitating conditions are factors. Now a day UTAUT is very much applicable to analyse the social impact, attitude, satisfaction of customers towards any banking service (5).

Methodology

1. Phase-I: Select a group of people who use Internet banking of IBBL.

2. Phase-II: Prepare questionnaire and divide the whole population into some sub group according to their age, education, profession, gender and residential status.

3. Phase-III: Using Data analysis methods and techniques.

Source of data

Here the author used primary data, collected from face to face interview. This primary data will be used to reach a persuasive outcome.

Collection of data

Here the author collected primary data through Structured Questionnaire, Personal Interview and group Discussion.

Data analysis

Data processing method

Some manual techniques will be applied during the collection of opinion through the questionnaire. First select the account holders of IBBL who use Internet banking, who has an valid e-mail ID and some knowledge in English and Basic computer skill. Then ask them some questions about how they are happy to use Internet banking interms of E-Commerce transaction and how much the customers of IBBL face problem to E-commerce transaction through Internet banking system of IBBL.

Here the author used questionnaire to evaluate the impact of internet banking of E-Commerce related transaction. The author took interview of 392 customers via face to face.

According to the TAM & UTAUT perceived ease of use and perceived benefits, perceived usefulness, social influence, satisfaction are the primary motivational factors for accepting and using new technologies. Based on these variables in TAM & UTUAT the following hypotheses were formulated:

Ho1: There is no notable association exists between perceived ease of use and attitude of customers towards using Internet banking in E-commerce transaction.

Ho2: There is no notable association exists between perceived usefulness and attitude of Customers towards using Internet banking system.

Ho3: There is no notable association exists between customer’s attitude towards using the Internet banking system and their intention to use it.

Ho4: There is no notable association exists between age and customer’s intention to use an Internet banking system for E-commerce transaction.

Ho5: There is no notable association exists between the level of computer skill and intention to use Internet banking system of E-Commerce transaction.

Ho6: There is no notable association exists between customer satisfaction and attitude of Customers towards using Internet banking system.

Ho7: There is no notable association exists between social impact and intention of Customers towards using Internet banking system.

Ho8: There is no notable association exists between gender and their attitude towards the benefit of Internet banking.

Ho9: There is no notable association exists between employment status and their attitude towards the benefit of Internet banking.

Ho10: There is no notable association exists between residential status and their attitude towards the benefit of Internet banking.

Ho11: There is no notable association exists between device user and their attitude towards the benefit of Internet banking.

Ho12: There is no notable association exists between education level and mindset of customer towards internet banking.

Table 15. Computer literacy level of the customers of IBBL.

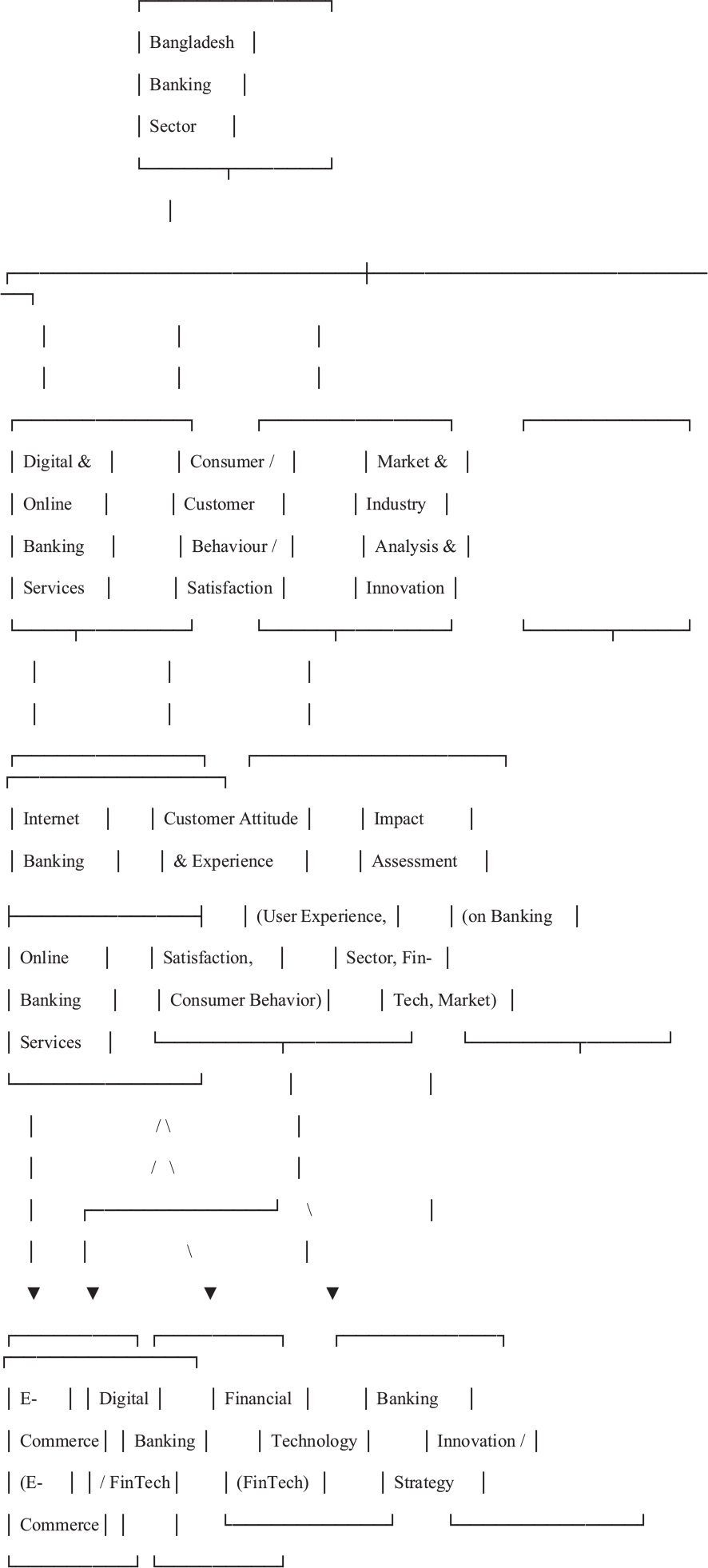

Conceptual diagram

The author recommend visualising a concept map / mind-map where central themes connect related subtopics. Below is a textual sketch of such a map/Diagram.

Interpretation of the diagram

E-Commerce, Internet Banking and Online Banking Services fall under the broader umbrella of Digital & Online Banking in the banking sector.

Digital Banking and Financial Technology (FinTech) act as enablers facilitating internet banking, e-commerce payments, and other modern banking services.

On the “consumer side,” Consumer Behavior, Customer Attitude, UX and Customer Satisfaction show how customers respond to and perceive these services.

At the macro level: Market Analysis, Banking Innovation and Impact Assessment deal with how digital banking and fintech transform the Bangladesh Banking Sector and influence the overall financial services landscape.

Financial Services acts as a broad container for all banking, lending, payments, and fintech-enabled services.

Here’s a side-by-side comparison focusing on digital banking, fintech adoption, customer reach, and innovation for IBBL vs. Sonali Bank.

DIAGRAM.

Interpretation & key insights

IBBL appears more “fintech-forward” among the two — with a robust digital banking app (Cellfin), virtual-card services, QR-payments, and aggressive use of fintech + traditional banking infrastructure to reach customers (urban + rural).

Sonali Bank , being a state-owned large traditional bank, is transforming steadily: using digital wallet, payment gateway, QR-withdrawals etc., but balancing between legacy branch-based banking and digital innovation — the strength lies in accessibility (especially for under-banked, expatriates), social-safety-net services, and regulatory/government-driven initiatives.

Their cooperation (IBBL using Sonali Payment Gateway) shows a hybrid model: a private bank leveraging a state-owned bank’s gateway to extend service— reflecting how digital banking services & fintech can foster cooperation, increase interoperability, and benefit customers.

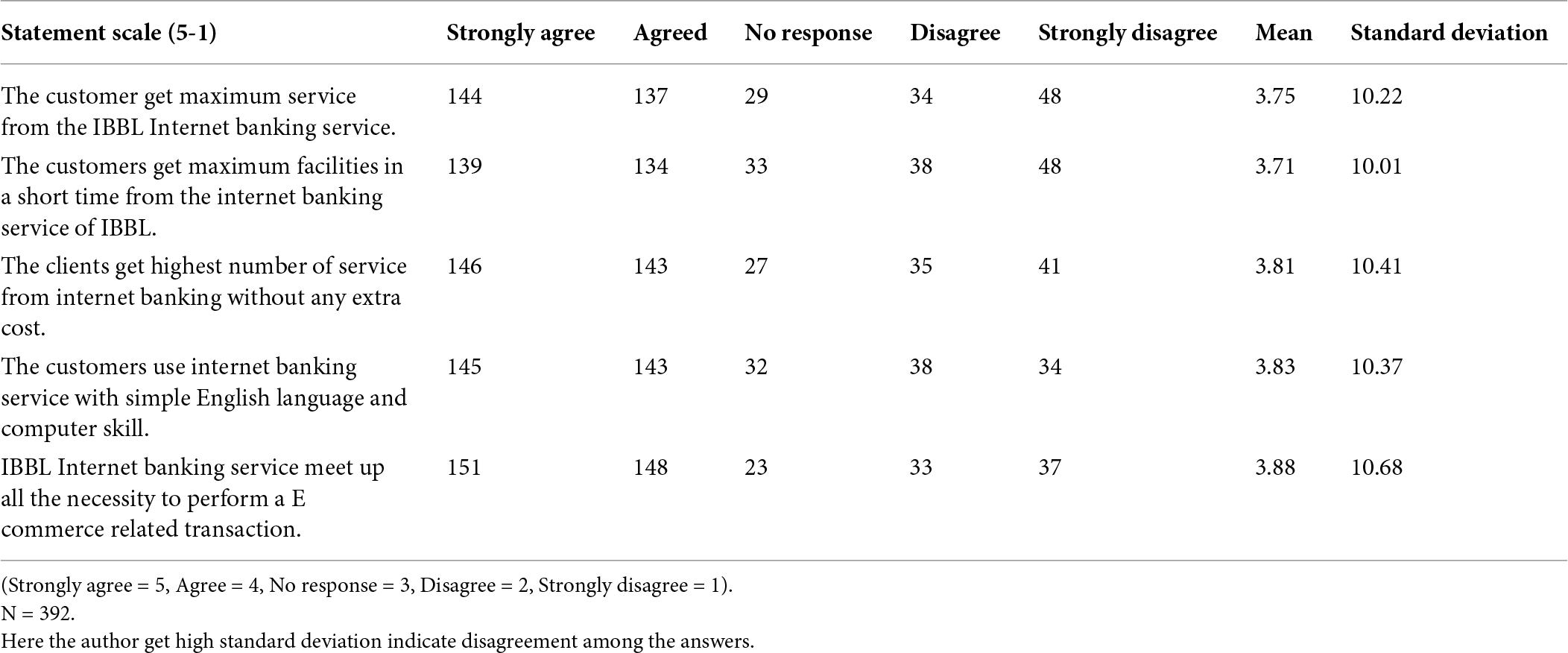

Table 16. Customer satisfaction towards internet banking service of IBBL.

Table 17. Customer satisfaction & attitude towards internet banking.

Data analysis

The population used in this research are people with a sample 392 customers scattered across all over Bangladesh. Samples were selected by intentional random sampling using a 1-5 Likert scale questionnaire. Research data analysis is performed by using Simple Linear Regression Analysis, One way ANOVA Test, F -Statistic, Chi-Square test. Respondents were then conducted to questionnaire, where they completed a questionnaire about their experience Internet banking of Islami Bank Bangladesh Ltd. All questionnaires are autonomous. The testing process was finalized when the respondents completed their responds.

Here the author used quantitative descriptive research method.

The range of interpreting the Likert scale mean score is as follows: 1.0–2.4 (Negative attitude), 2.5–3.4 (Neutral attitude), and 3.5–5.0 (Positive attitude).Here the author get high standard deviation indicate disagreement among the answers.

Table 18. Regression analysis of customer satisfaction & attitude towards internet banking.

Test of hypotheses

Hypothesis one

Ho1: There is no notable association exists between perceived ease of use and attitude of customers regarding Internet banking in E-commerce transaction.

Table: Here the author used simple linear regression analysis to find out the association between perceived ease of use and attitude of customers towards using Internet banking in E-commerce transaction.

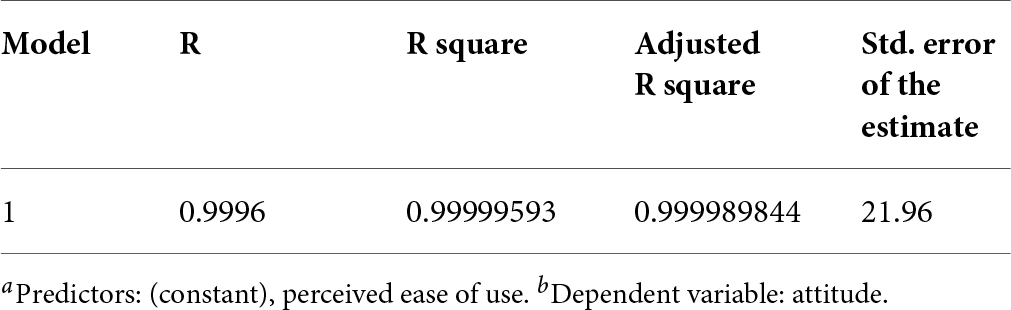

Outcomes in Table 5 express that there is a remarkable association exists between perceived ease of use and attitude of customer’s regarding internet banking, that is, (P = 0.00 < 0.05). The Beta value (r = 0.9996) disclose that there is a strong positive correlation exists between attitude and perceived ease of use. The R Square prove that 0.99999593 of the total variation of attitude is interpreted by perceived ease of use. On that basis therefore, the null hypothesis is accepted, and the alternative rejected.

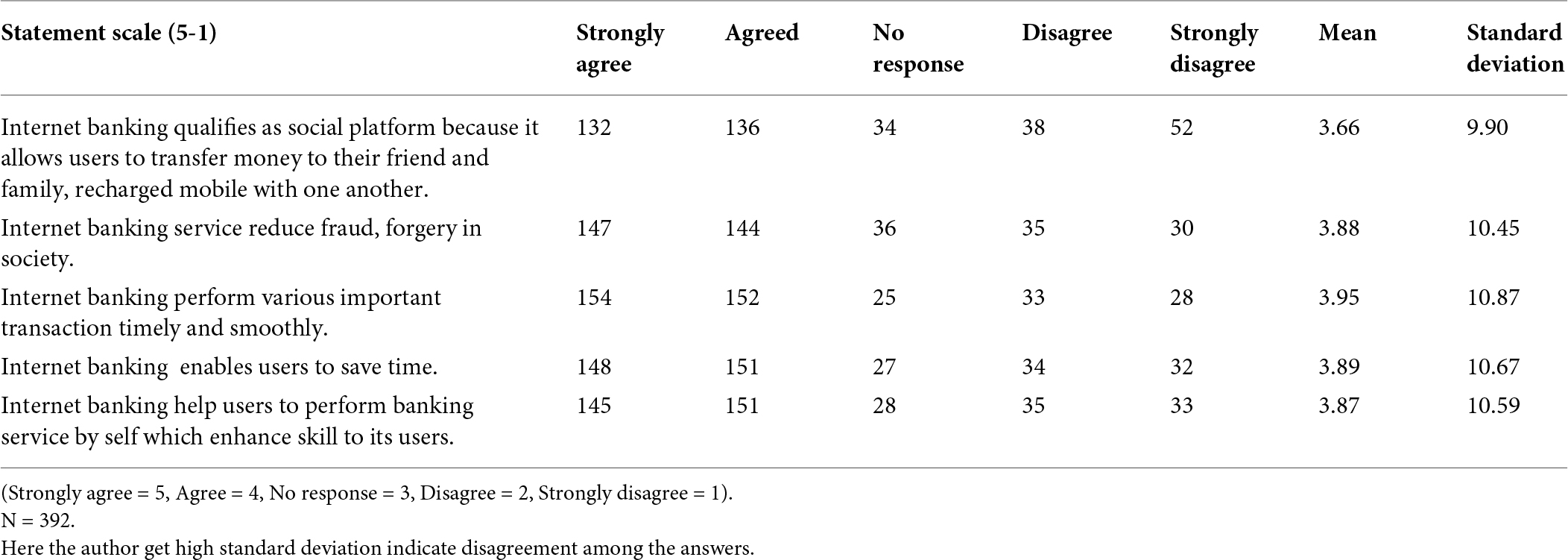

Table 19. Social impact of internet banking.

Table 20. Association between social impact and intention of customers towards using internet banking system.

Ho2: There is no notable association exists between perceived usefulness and attitude of Customers towards using Internet banking system.

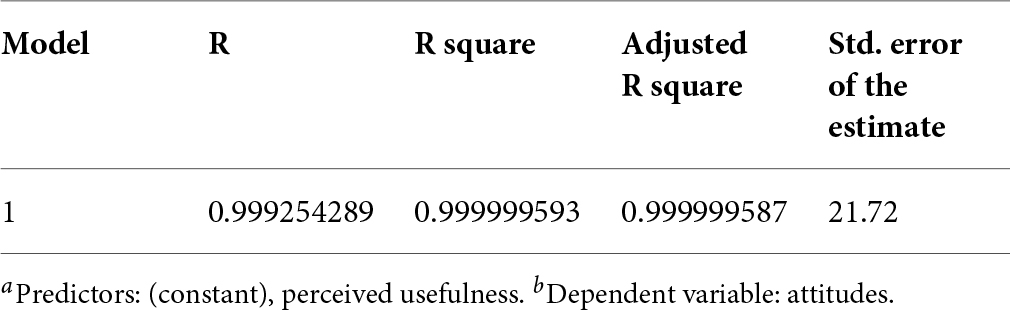

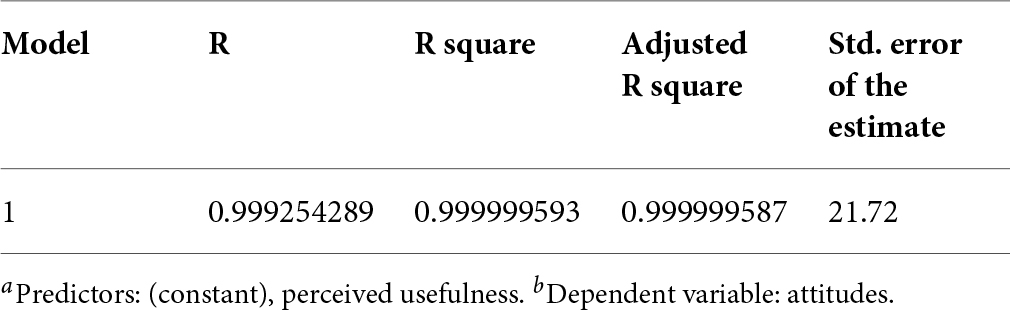

Outcomes in Table 8 show that there is a significant association exists between perceived Usefulness and attitude of customer’s regarding the use of internet banking, again (P = 0.00 < 0.05). The beta value (r = 0.999254289) also disclose that there is a strong relationship between attitude and perceived usefulness. The R Square disclose that 99.99% of the total variation of attitude is interpreted by perceived ease of use. Thus, it can be concluded that there is a positive relationship between Attitude of customers and their perceived usefulness of internet banking. On that ground, the null hypothesis is accepted and the alternative rejected.

Ho3: There is no remarkable association exists between customer’s attitudes regarding Internet banking system and their intention to use it.

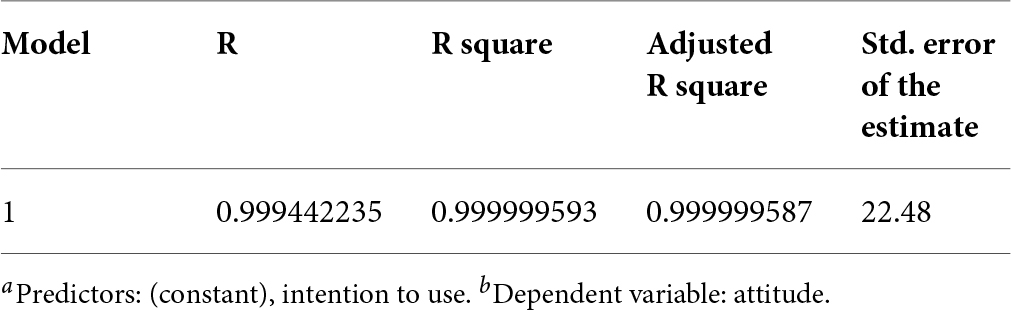

The results presented in Table 10 show that there is a significant relationship between attitude and the intention to use internet banking again here (P = 0.00 < 0.05). The beta value (r = 0.999442235) in table reveals that there is a strong positive association exists between attitude and the intention to use internet banking. The R Square value reveals that 99.99 % of the total variation of attitude is explained on the intention to use internet banking. The null hypothesis is therefore accepted and the alternative rejected.

Table 21. Regression analysis social impact and intention of customers towards using internet banking system.

Table 22. Demographic attributes of the customers.

Ho4: There is no notable association exists between Age and customer’s intention to use an Internet banking system for E-commerce transaction.

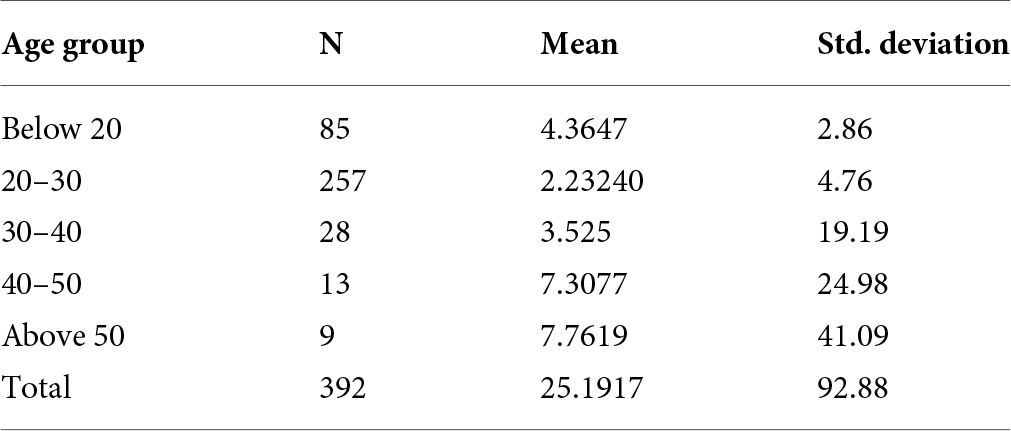

The consequences in Tables 12 and 13 represent that there is no notable association exists between age of respondents and their intention to use internet banking system. Because the P-value of 0.814 is larger than the P table value (P = 0.814 > 0.05) Based on the decision rule the author anticipated to accept the null hypothesis and reject the alternative hypothesis. The table showed that the age group (Above 50) has the largest mean of 7.7619 although the age group of (20–30) has the lowest mean of 2.23240.

Table 23. Gender vs. attitude.

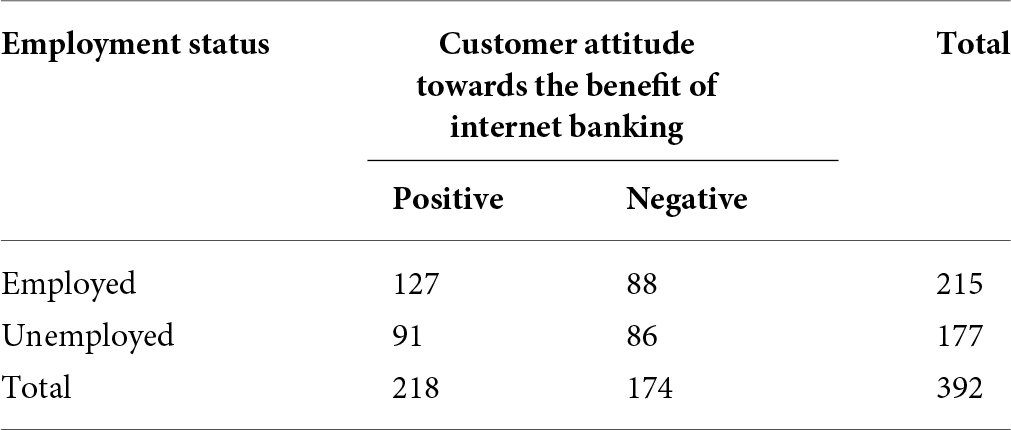

Table 24. Employment status vs. attitude.

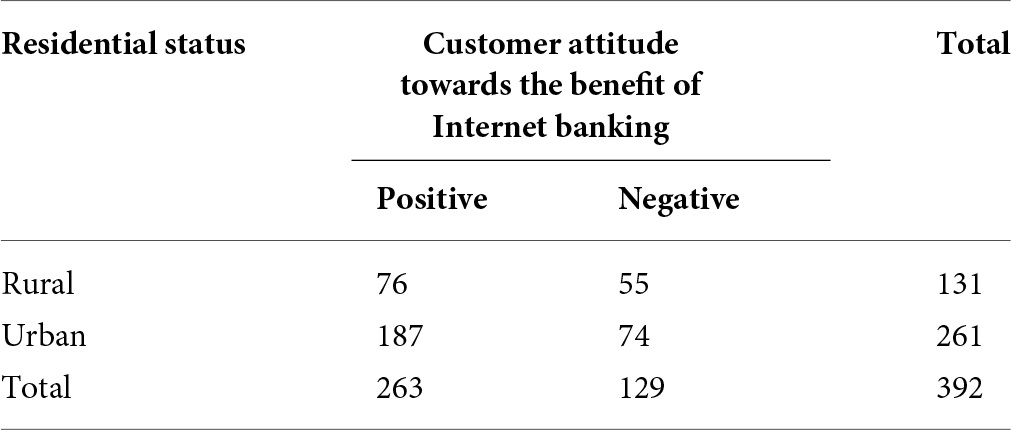

Table 25. Residential status vs. attitude.

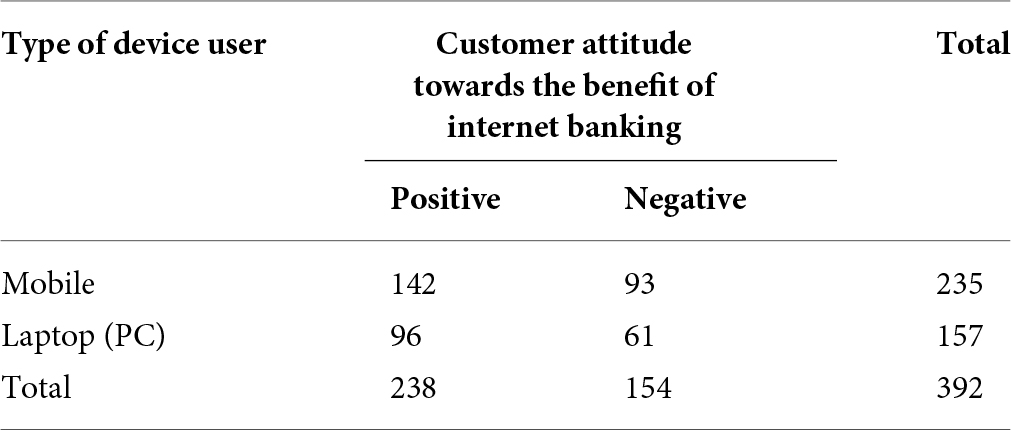

Table 26. Device type vs. attitude.

Hypothesis five

Ho5: There is no significant relationship between the level of computer literacy and customer’s intention to use internet banking.

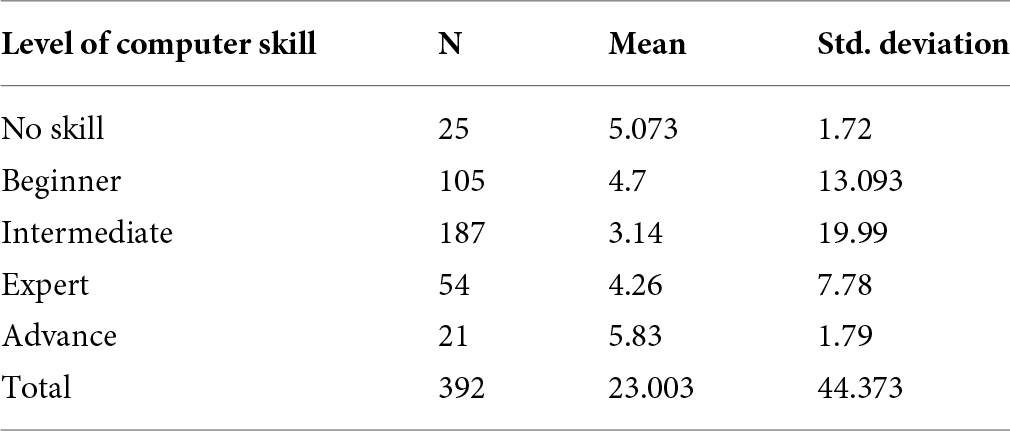

The outcomes in Tables 14 and 15 showed that there is no remarkable association exists between level of computer experience and their intention to use an internet banking system. Because here P = 0.252 > 0.05.As a consequence the author accept the null hypothesis which states that there is no significant relationship between level of computer skill and the intention to use an internet banking system and also the researcher reject the alternative hypothesis. The table showed that respondents in the advanced level of computer experience comprised the highest mean of 5.83, on the other hand the respondents with Intermediate level of computer skill composed the lowest mean of 3.14.

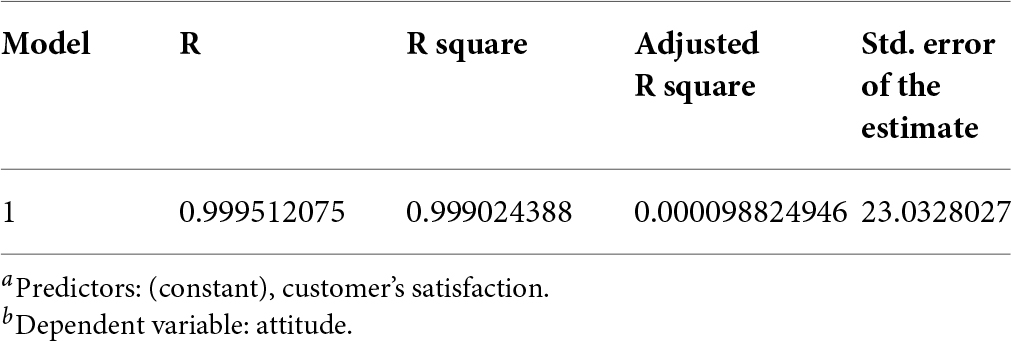

Null Hypothesis 06: There is no notable association exists between customer satisfaction and attitude of Customers towards using Internet banking system.

Outcomes in Table 8 represent that there is a notable association exists between customer’s satisfaction and attitude of customer’s towards the use of internet banking service, because (P = 0.00 < 0.05). The beta value (r = 0.999512075) also proved that there is a strong relationship between attitude and customer’s satisfaction. The R Square disclosed that 99.99% of the total variation of attitude is interpreted by satisfaction. As a consequence, it can be said that there is a positive association exists between Attitude of customers and their satisfaction of Internet banking systems. On that basis, the null hypothesis is accepted and the alternative is rejected.

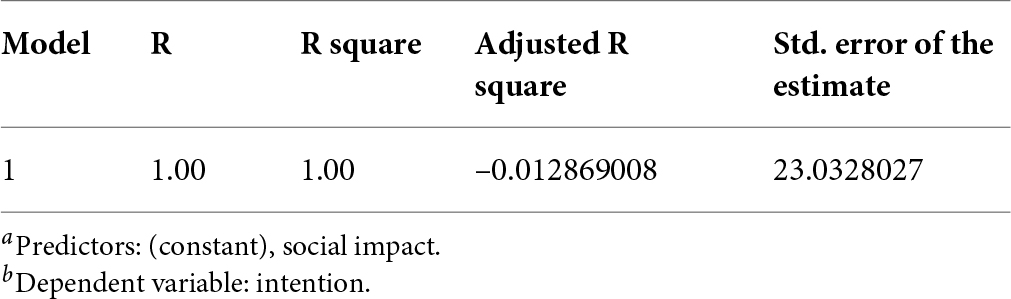

Null Hypothesis 07: There is no notable association exists between social impact and intention of Customers towards using Internet banking system.

Consequences of Table 8 represent that there is a notable link exists between social impact and intention of customer’s towards the use of Internet banking system, because (P = 0.00 < 0.05). The beta value (r = 1) also showed that there is a strong association exists between Intention and social impact. The R Square prove that 100% of the total variation of Intention is interpreted by social impact. As a consequence, it can be established that there is a positive association exists between Intention of customers and social impact of Internet banking systems. On that ground, the null hypothesis is accepted and the alternative rejected.

Table 27. Education level vs. mindset.

Goodness of fit-test

Null Hypothesis 08: There is no significant relationship between gender and their attitude towards the benefit of Internet banking.

Here the author used Chi Square test,

The calculated Chi-square value is = 0.099450315.

So chi square cal < chi square table.

So the null hypothesis, there is no significant relationship between gender and their attitude towards the benefit of Internet banking is not rejected or it is true.

Null Hypothesis 09: There is no significant relationship between employment status and their attitude towards the benefit of Internet banking.

Here the author used Chi Square test,

The calculated Chi-square value is = 2.303656049.

So chi square cal < chi square tab.

So the null hypothesis, there is no significant relationship between employment status and their attitude towards the benefit of Internet banking is not rejected or it is true.

Null Hypothesis 10: There is no significant relationship between residential status and their attitude towards the benefit of Internet banking.

Here the author used Chi Square test,

The calculated Chi-square value is = 7.341146075.

So chi square cal ¿ chi square table.

Here the null hypothesis, there is no significant relationship between residential status and their attitude towards the benefit of Internet banking is rejected or not true. So there is a significant relationship exists between residential status and their attitude towards the benefit of Internet banking.

Null Hypothesis 11: There is no significant relationship between device user and their attitude towards the benefit of Internet banking.

Here the author used Chi Square test,

The calculated Chi-square value is = 0.020597267.

So chi square cal < chi square table value.

So the null hypothesis, there is no significant relationship between device user and their attitude towards the benefit of Internet banking is not rejected, or it is true.

Null Hypothesis 12: There is no significant relationship between education level and mindset of customer towards internet banking.

Here the author used Chi Square test,

The calculated Chi-square value is = 16.64608438.

So chi square cal ¿ chi square tab.

So the null hypothesis, there is no significant relationship between education level and mindset of customer towards internet banking is rejected or not true. There is a significant relationship exists between education level and mindset of customer towards internet banking.

Validity test

Content validity

For content validity test purpose the author give questionnaire to customers,

where Ne = number of experts voting essential,

N = total number of recruited experts.

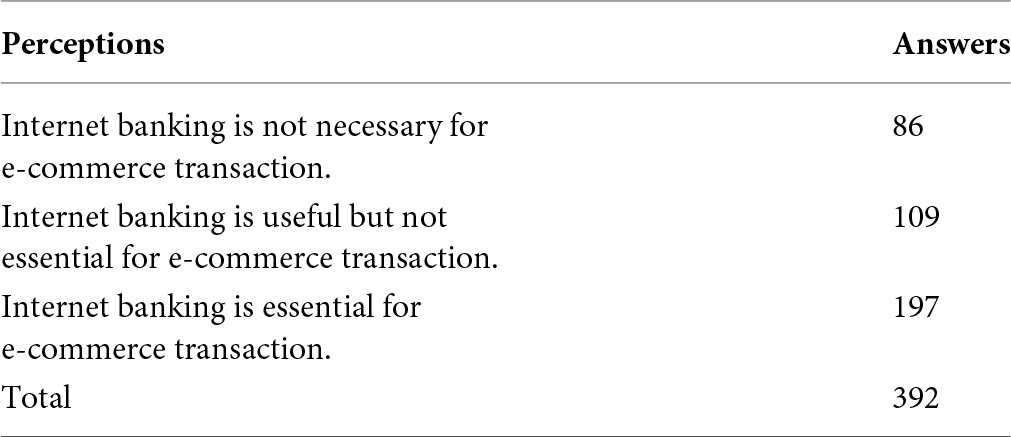

Now, Content Validity Rate = (197–196)/196 = 0.0005103040816.

This formula yields values which range from +1 to -1; positive values indicate that at least half the respondents rated the item as essential.

Convergent validity

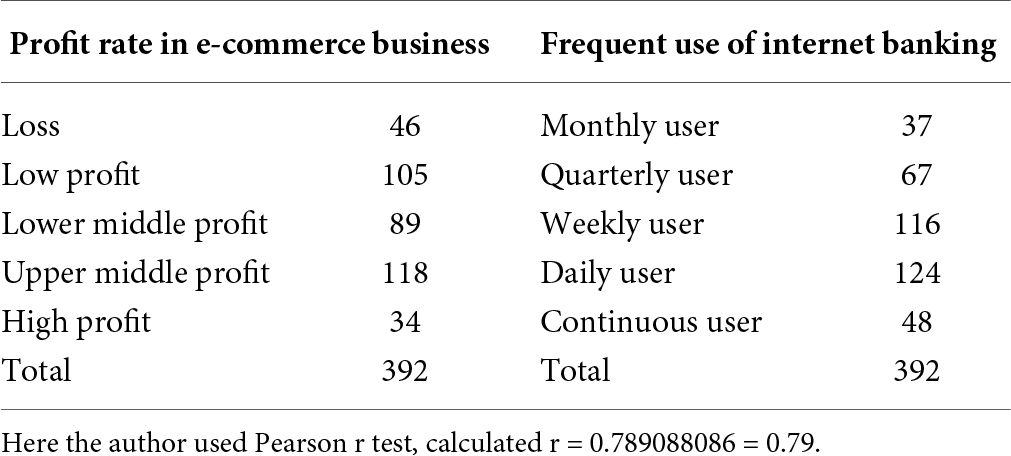

To measure Convergent Validity the author used two related scale such as make profit in E-commerce business and frequent use of internet banking.

Convergent validity is generally considered adequate if ¿75% of hypotheses are correct. So the test is adequate.

Discriminant validity

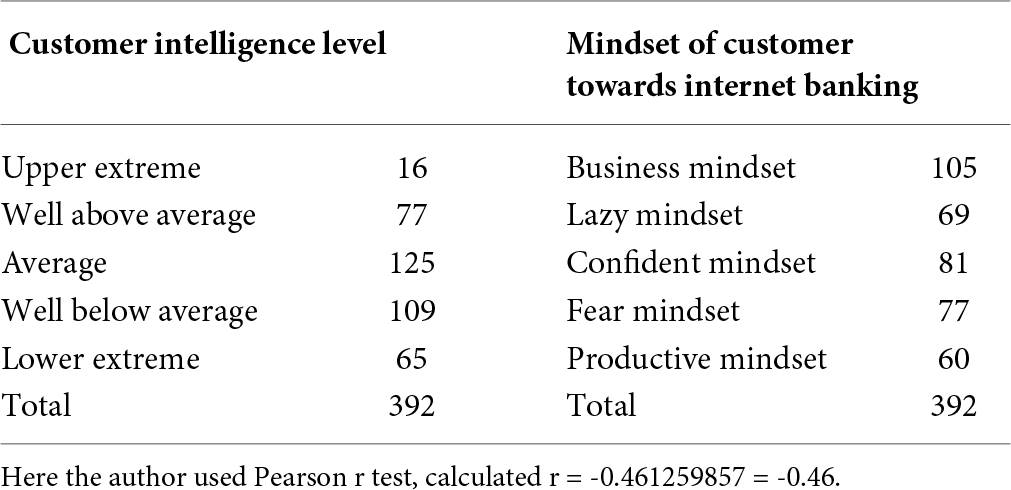

For testing Discriminant Validity the author respondents to fill in a second questionnaire measuring intelligence in order to test the discriminant validity of his questionnaire. Here the author try to construct a relationship between customer’s intelligence and mind set of customer’s towards internet banking.

The author get r value is negative, it also seems to match his/her expectation about the relationship of the constructs, which is good.

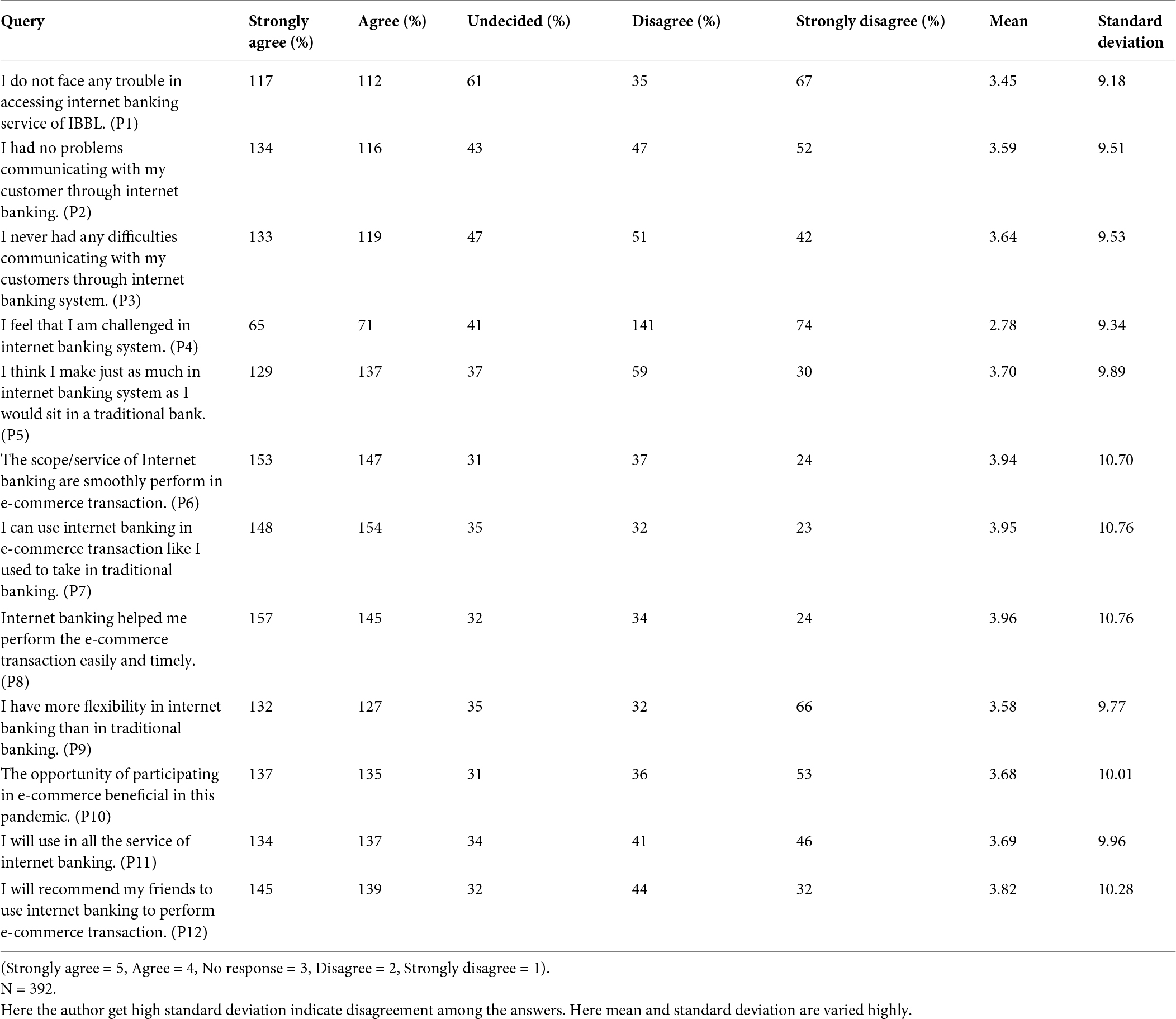

Table 28. Descriptive statistics of the twelve Likert scale items.

Discussion & result

In Table 1, the author represents a comparative analysis between Islami Bank and Sonali Bank of Bangladesh in terms of net banking service. From the data analysis section of the paper the author found that (Table 2) most of the customer agreed that perceived ease of internet banking is high. Again most of customers replied e that perceived use fullness of internet banking service of IBBL is appreciable (Table 3). The research found that maximum of the customers have positive intention towards internet banking service of IBBL (Table 4). Here the author also showed that (Table 5) most of the customers have positive attitude towards internet banking service.

In the above study the situation explains about, there is an association exists between perceived ease of use and attitude of customers of IBBL to perform E-Commerce transaction through Internet banking. In this research the Beta value (r = 0.9996) represent that there is a strong positive correlation exists between attitude and perceived ease of use (Table 6). Again in this research the R Square disclose that 0.99999593 of the total variation of attitude is interpreted by perceived ease of use, so the null hypothesis is, there is no notable association exists between perceived ease of use and attitude of customers regarding Internet banking in E-commerce transaction is accepted (Table 7).

Association is a concept, but correlation is a measure of association and mathematical tools are provided to measure the magnitude of the association. So ease of use of Internet banking cant affect their attitude towards Internet banking.

Again in this research the author found that (Table 8) there is no remarkable association between perceived usefulness and attitude of Customers towards using Internet banking system is true. So if the customers don’t get enough usefulness through Internet banking its has on effect on the attitude of customers.

The author also found that (Table 10) there is no notable association between customer’s attitudes towards using the Internet banking system and their intention to use it is true. But the beta value (r = 0.999442235) in table reveals that there is a strong positive relationship between attitude and the intention to use internet banking of IBBL. This two opposite statement explain that customer’s attitude and their intention to use Internet banking are strongly positively correlated but customer’s aggressive attitude or politeness can’t affect their intention to use Internet banking for E-Commerce transaction.

In this research the author also found that, there is no remarkable association exists between age and customer’s intention to use an Internet banking system for E-commerce transaction is true (Table 12). So customers at different age can frequently used Internet banking service to perform E-Commerce transaction. So customers at different age can smoothly used Internet banking service.

This research also show that (Table 14) there is no notable link exists between the level of computer literacy and customer’s intention to use internet banking is true. So level of computer skill of customer’s can’t affect their intention to use Internet banking system to perform E-Commerce transaction. So very simple and basic computer skill required to perform Internet banking transaction service of Islami Bank Bangladesh Ltd.

The author showed there is a positive association that exists between perceived usefulness and attitude of customers towards internet banking service (Table 9). The research also express that there is no notable association exists between customer satisfaction and their attitude towards internet banking (Table 17). So if the customer is less satisfied by internet banking service it could not mean they use less of internet banking system.

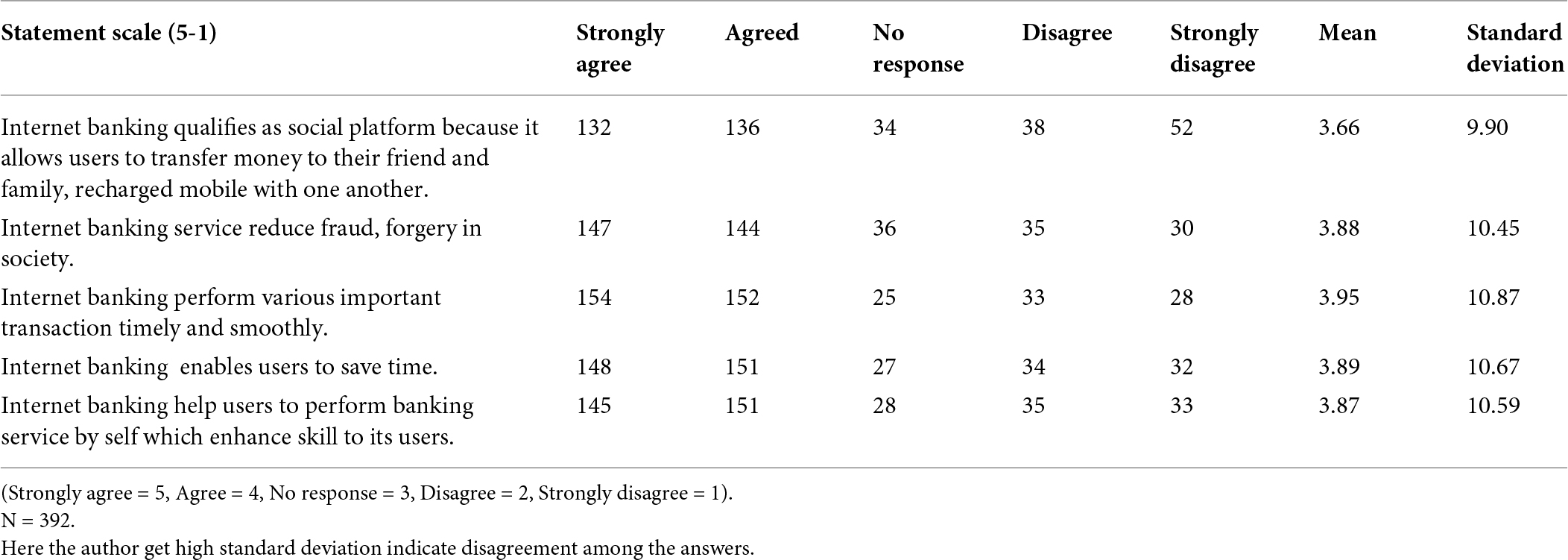

In Table 11, the author showed that there is a positive relation that exists between the attitude and intention of customers towards the internet banking service of IBBL. Here the researcher also discusses the social impact of internet banking of IBBL (Table 19). Most of the customers agreed that that internet banking has positive social impact.

From this research we found that internet banking service of IBBL has a positive social influence (Table 20). The research also show that social impact and customer intention have no significant relationship. So if social impact of internet banking service is reduced which can’t decrease the intention of customers towards internet banking.

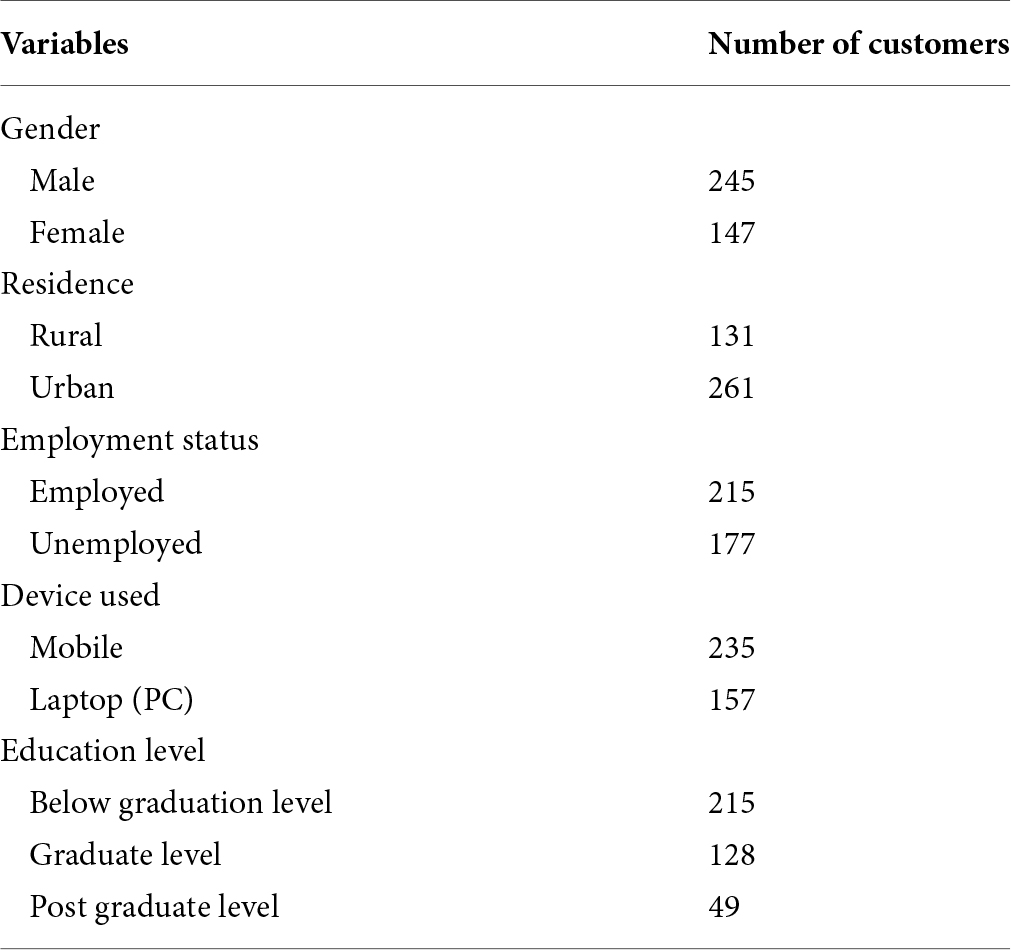

In this paper the author also explains the demographic attributes of the respondents (Table 22). In the research 245 male and 147 female are participated. In this research urban respondents are more than rural. The research found that maximum of the respondents use mobile device to access internet banking than laptop. In this research maximum of the respondents education level is below graduation level.

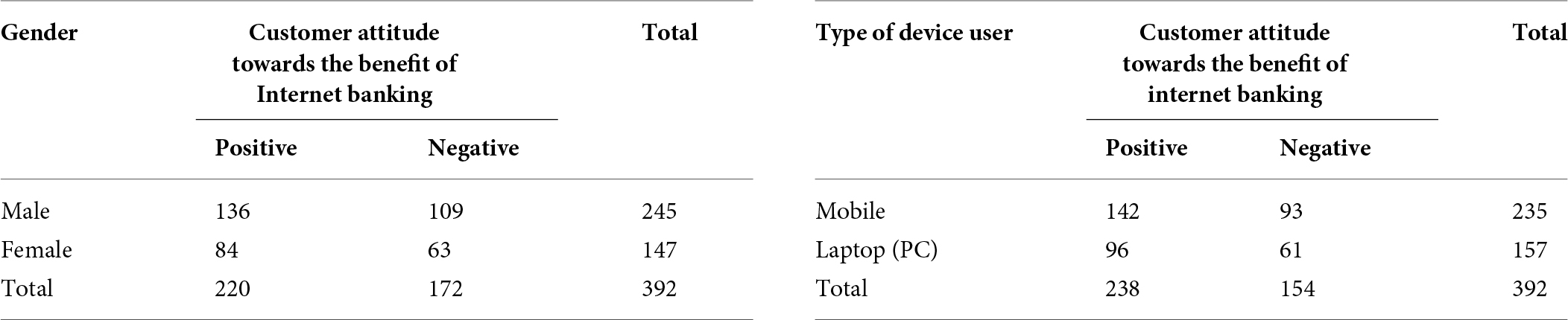

The research also developed that there is no remarkable association exists between gender and attitude of customers to the benefit of internet banking (Table 23). That means maximum of male and female have a positive attitude to the benefit of internet banking service.

The research also found that there is no significant relationship between employment status and their attitude towards internet banking (Table 24).

In Table 16, the author represents customer satisfaction towards the internet banking service of IBBL. In this table the author found that most of the customers express great satisfaction with the internet banking service of IBBL. The research also shows that (Table 25) residential status and attitude of customer towards internet banking are significantly related. Urban people have more positive towards internet banking because network facilities system is weak in the rural area of Bangladesh.

The research also shows that there is no significant relationship between device user and their attitude towards internet banking. Access of internet banking and operating it through different device like mobile, laptop is same (Table 26).

In Table 18, the author showed that there is a positive relation that exists between customer satisfaction and attitude towards internet banking. The research also establishes that there is a significant relationship between education level and mindset of customers towards internet banking (Table 27).

In 12 Likert scale mean is greater than 3 represent a positive attitude of customers of Islami Bank Bangladesh Ltd towards Internet banking. High Standard deviation indicates there was a wide range of answers, indicating disagreement (Table 28).

In Table 21, the author represents that a positive regression exists between social impact and intention of customers towards using the internet banking system. For validity test purpose the author shows that, the content validity proved that half of the customer rated that the internet banking service is essential to perform E-Commerce related transaction (Table 29). Convergent Validity shows that the internet banking service is adequate to perform e-commerce related transaction (Table 30). In this research the discriminant validity has a negative value. For the discriminant validity purpose the author selects two criteria such as customer’s intelligence level and mind set of customer’s towards internet banking (Table 31). Here the author used Pearson r test, which gives a negative value (-0.46). So intelligence level is negatively related to the customer’s mindset.

Internet banking payment systems of IBBL still require less time for validation and payment steps. So this is very less time-consuming service.

Again electronic fund transfer (EFT) transaction through Internet banking faces some problem also, such as the clients cannot reverse the transaction if any error occurs, sometimes they may not get any confirmation message of successful EFT transaction. But NPSB provide quick service for performing E-Commerce related transaction.

Although a large number of clients of IBBL get satisfied to using Internet banking service to perform E-Commerce related transaction. So in Bangladesh the people can perform E-commerce related transaction smoothly through Internet banking service of Islami Bank Bangladesh Ltd.

Table 29. Significance of internet banking.

Table 30. Profit vs. frequency.

Table 31. Intelligence vs. mindset.

Conclusion

Internet network is the main mode to perform net banking which is a very reliable payment system in the whole world. The Internet banking service makes different payment method very easy with different and distance location. By using this payment system customers don’t need to worry about any kind of cheating.

The research showed that internet banking service of IBBL has greatly influenced the E-commerce related transaction in Bangladesh.

Benefits of e-commerce incorporate helping one to select from a wide range of products and get the order delivered too. Looking for a product, seeing the description, adding to cart – all steps happen in a flash precisely. Finally the customers are happy because they have the item and didn’t have to travel far. Islami Bank Bangladesh Ltd play an important role to perform E-Commerce transaction through Internet banking.

Islami Bank Bangladesh Ltd made it easy to handle customer’s issue in performing E-commerce related transaction by setting up a strong server system, adding various service system like NEFT, RTGS, EFT, NPSB, Fund transfer, IMPS in internet banking service of IBBL. Islami Bank Bangladesh Ltd establishes a strong security system, password protection system, two factor authentication system to protect transaction through internet banking.

The author also found that the internet banking service of IBBL is more effective and user friendly than others bank like Sonali bank of Bangladesh.

Internet banking service of IBBL is very easy to registered and access, it’s required very simple English language and simple computer skill to login and do transaction through internet banking So IBBL expanded the internet banking service all over Bangladesh and enhanced its acceptability among all type of customers by making the internet banking service easy and useful.

Funding

The author declares that this research received no external funding.

Conflicts of interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

1. Alsajjan B, Dennis C. Internet banking acceptance model: cross-market examination. J Bus Res. (2010) 63(9–10):957–63.

2. Lee MC. Factors influencing the adoption of internet banking: an integration of TAM and TPB with perceived risk and perceived benefit. Electron Commer Res Appl. (2009) 8(3):130–41.

3. Foon YS, Fah BCY. Internet banking adoption in Kuala Lumpur: an application of UTAUT model. Int J Bus Manag. (2011) 6(4):161.

4. Venkatesh V, Morris MG, Davis GB, Davis FD. User acceptance of information technology: toward a unified view. MIS Q. (2003) 27(3):425–78. doi: 10.2307/30036540

5. Davis FD. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q, (1989) 13(3):319–40. doi: 10.2307/249008

6. Lewis R, Dart M. The New Rules of Retail: Competing in the World’s Toughest Marketplace. Palgrave Macmillan (2010).

7. Martins C, Oliveira T, Popoviè A. Understanding the internet banking adoption: a unified theory of acceptance and use of technology and perceived risk application. Int J Inform Manag. (2014) 34(1): 1–13.

8. Hanafizadeh P, Keating BW, Khedmatgozar HR. A systematic review of Internet banking adoption. Telemat Inform. (2014) 31(3): 492–510.

9. Yousafzai S, Pallister J, Foxall G. Multi-dimensional role of trust in Internet banking adoption. Serv Ind J. (2009) 29(5):591–605.

10. Özkan S, Bindusara G, Hackney R. Facilitating the adoption of e-payment systems: theoretical constructs and empirical analysis. J Enterp Inform Manag. (2010) 23(3):305–25.

11. Kesharwani A, Singh Bisht S. The impact of trust and perceived risk on internet banking adoption in India: an extension of technology acceptance model. Int J Bank Market. (2012) 30(4):303–22.

© The Author(s). 2026 Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.