Introduction

As a more general framework, the international risk management task is vastly broader than tracking spot exchange rates but must also be concerned with how conditions monetary and other aggregate through investor risk-taking (risk appetite) and corrective policy reactions into price movements. All about the classical: Uncovered Interest Rate Parity (UIP): essentially, higher-yield currencies need to depreciate in order for arbitrage profits to be wiped out. But the reason why carry trade returns survive and the interesting rate-differential models empirically fail to deliver reliable predictions of exchange rate changes has long suggested that the interest rate-exchange rate relationship is contingent, noisy, and risk-premia dominated rather than being mechanical adjustments toward (interest-rate) parity (1). The significance of recent research on foreign exchange behavior and its expressions in connection to actual risk management by multinational corporations and financial institutions is examined in this study.

Objectives

• To investigate the implications of interest rate differentials on international foreign exchange risk management.

• To demonstrate the limitations of Uncovered Interest Rate Parity (UIP) in explaining observed movements in exchange rates.

• To serve as evidence for how much time-varying risk premia, yield-curve factors, the behavior of investors, and volatility in markets affect currency movements.

• To detect high-yield currency exposures that dodge asymmetric reactions (including crash risk and extreme depreciation risk).

• Explains why the volatility of exchange rates changes throughout market regimes (crisis vs. post-crisis phases).

• To examine the influence of the central bank’s policy responses and then exchange rate pressure on the process in interest rate-exchange rate dynamics

• The possible persistence of structural exchange rate misalignment and its propagation through capital flows, interest differentials, and external macroeconomic conditions.

• To acknowledge the necessity of recommending adaptive, state-dependent FX risk management strategies as opposed to static hedging or mechanical parity assumptions.

• To explain forwards, futures, and options, scenario analysis, and stress testing as tools for managing currency risk.

Methodology

This paper employs a qualitative literature review approach based on five selected journal articles. Interest rate differentials change exchange rate behavior and affect the practices of foreign exchange risk management, which were reviewed through journals. Using a thematic analysis, the study explores underlying key themes such as risk premia, exchange rate volatility, carry trade risk, central bank policy reaction, and long-term currency misalignment.

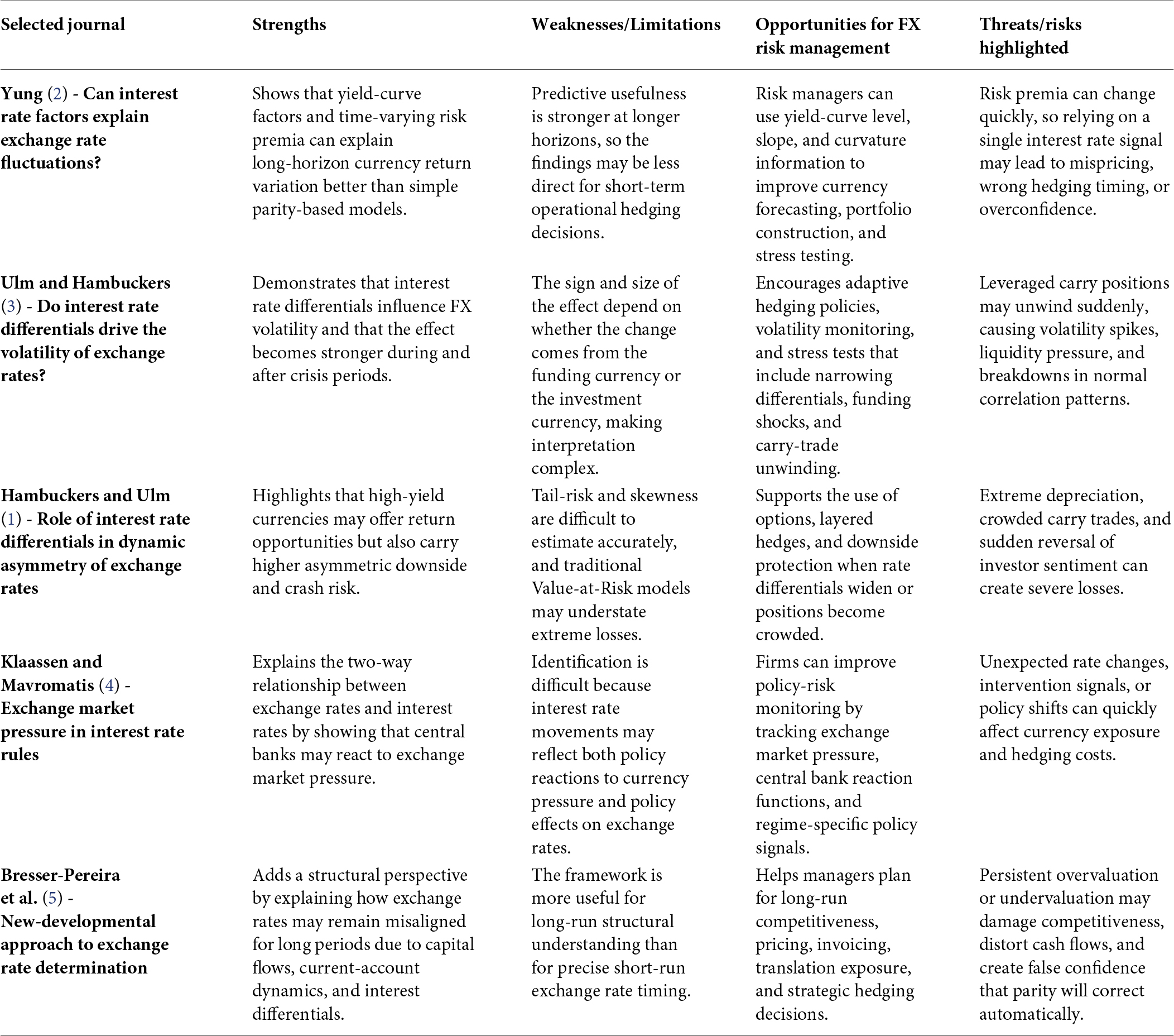

SWOT analysis from the five selected journals

Refer to Table 1 for additional information.

Table 1. SWOT Analysis of the five selected Journals.

Rethinking theory: from parity conditions to risk premia

One of the main reasons UIP is so attractive is it provides a strong prediction—namely that changes in exchange rates should be related to interest rate differentials. Yet we learn from the “UIP puzzle” that being equal is a good first approximation, but also this must be weighted with other factors like risk-based pricing or segmented markets not off-market views as to their distance to it. Other recent work here builds on that with more precision: embedding exchange rates within asset-pricing frameworks. The bulk of long-horizon variation in currency returns is accounted for by time-varying risk premia embedded in yield-curve factors, especially the level, slope, and curvature, as shown by Yung (2). Which translates to the following conclusion for that theory: it tells an old story in a new language; interest rates matter not through profitability expectations but together with a dynamic of stochastic discount factors and risk premia on stock exchange rates (2).

The implication of that insight is one of several implications but the most important: “the interest rate”—it is not pure substance. In other words, short rates are the policy stance, and the term structure reflects market expectations and risk pricing going forward. But if the exchange rate does respond to global risks, local risks, and domestic economic fundamentals, as a good number of estimates suggest, then sufficiently different maturities will induce currency floats even without changes in monetary policy. This is also the reason for the otherwise mysterious failure of simple parity regressions that turns a multi-factor pricing relation into a single one and implicitly treats risk premia as constant.

What the evidence actually says

Three themes that this task extracts from the journals deserve some empirical attention. First, while rate differentials continue to provide information (maintain their mean depreciation role), this has been the case for many of its risk and distributional features. Dynamic asymmetry relates to the difference in interest rates: while statistically, a high-yield currency may be expected to appreciate, as this differential increases, so does the risk of extreme depreciation proportional to a corresponding probability scale, according to Hambuckers and Ulm (1). This “crash-risk trade-off” is well-acquainted with the notion of carry returns as compensation for exposure to skewness and kurtosis (1).

Second, interest rates are regime-dependent and affect exchange rate volatility accordingly. Ulm and Hambuckers (3) demonstrate that variations in interest rate differentials can redistribute aggregate FX volatility, particularly during and following periods of crises, consistent with the unwinding of leveraged carry positions. And the sign and the magnitude depend on whether the adjustment comes from a funding- or an investment-currency rate, which emphasizes that “narrowing differentials” is not one mechanism but rather a collection of balance-sheet and flow responses (3).

Third, the interest rate–exchange rate link is mediated by the policy environment. Klaassen and Mavromatis (4) formalize the notion of many central banks responding to exchange market pressure by changing interest rates, which means that exchange rate management becomes part of the reaction function. This is complicated for an empirical interpretation: the relationship between rates and currency pressure (in both directions) is much more complex than “rates → FX” alone, providing a new impetus to explore “FX conditions → rates” (4).

A more general critique is presented by Bresser-Pereira et al. (5), who argue that the exchange rate can be misaligned for extended periods of time, a flight-forward mechanism driven by capital flows and interest differentials in addition to terms of trade and current-account dynamics. This assumption has proven to be extremely misleading since it implies that exchange rates return to a (fundamental) level and guides risk managers during episodes of prolonged overvaluation/undervaluation towards the belief that “parity will be reached in due time” (5).

Advanced critical reflection: what these studies leave unresolved

The journals all confirm the last point—that, at some level, interest rates do impact beyond those risk premia and volatility and policy reaction functions. Despite the qualitude of a risk-focused read, and the neareast things that matter still exist.

First, identification remains difficult. Where local central banks are applying rate hikes in part to shore up a falling currency (as rules based upon exchange-market pressure would imply), conventional regressions risk embedding muddle between policy reaction and policy effect. In even simpler terms, the corollary is that countdown firms should not regard interest rate announcements as an exogenous shock that imparts information on the stress states of the underlying FX market (4).

The second thing is that by the horizon and the state, i.e., world state, these models are limited. Yung (2) demonstrates that this low-frequency predictability seems much stronger at long horizons, and Ulm and Hambucker (3) observe that during a crisis or after it, volatility effects increase. For the foreseeable future, any such “interest rate to FX” matrix is going to be very sensitive about what market structures do when it comes to changing leverage and risk appetites. This is a cautionary tale, in terms of risk, about hedging strategies fitted only to placid time periods: correlations and our need to care about volatility may change dramatically when carry trades unwind.

Third, focusing on distributional features (skewness, crash risk) also gives guidance on how to take measures of risk. Even if interests differentials increase to a tail, either alone or on top of tend to a reduction in variance, it will not do. Wide differentials and crowded positions are exactly where Value-at-Risk models understate exposure (1).

Finally, there is a tension in theory between “fundamentals” and “financial channels.” The development perspective emphasizes structural misalignment that is basically determined in terms of flows and policy flows; the volatility and asymmetry perspectives are more about how traders position themselves over relatively short horizons. This requires management of FX risk on two fronts: the risks posed both by long-run misalignment (pricing, competitiveness, cash-flow translation) and short-run liquidity/tail-risk episodes (margin calls, funding stress), as it is possible for these to infect each other and thus need to be managed in series.

Implications for managing international FX risk

Therefore, the main implication for MNCs is to re-evaluate this common notion that interest rate differentials are somehow “directional forecasts” of how spot rates go, where they do provide some value but only by a function of their risk environment. Differentials signal that they are becoming not only more likely to crash but also more volatile; thus, the hedging policy ought perhaps to be adaptive rather than static. Operationally it is a multi-layered trade, the first line manifestation of the defense stacking hedge at budget rates versus spot, then appendix protection that allows for tail events when the differentials blow out or convergence of policy disrupts carry.

The FX exposure hedging strategies use financial derivatives such as options (or foreign futures and forward markets) according to the literature on risk management (6). These papers represent empirical contexts for which each instrument is presumably most useful. If risk is mostly about interest rates and therefore risk shows up in terms of volatility (and specifically downside tails), this is precisely where options come into play because the payoff structure they offer is concave (they become your insurance against jumps in the underlying assets); a forward, on the other hand, will do nothing but hedge expected cash flows.

The implications for financial institutions are far-reaching and affect portfolio construction and stress testing. Yung (2)’s factor-based theory suggests that yield-curve data can be utilized to develop currency strategies beyond conventional carry signals. But the evidence of volatility and asymmetry warns that profits may be a reward for infrequent but extreme losses. Thus, risk governance should demand scenario analysis in which funding rates increase, differentials narrow, and volatility surges (3), not to mention extreme scenarios where high-yield currencies suffer a sharp depreciation (1).

The exchange-market-pressure framework, from a policy-risk perspective, suggests that interest rate moves may be motivated by the desire to protect exchange rate objectives. At the firm level, this suggests that policy monitoring should go beyond inflation and growth indicators and include signals of those managing the exchange rate (4). In such a regime where authorities are biased against depreciation, interest rate surprises should have greater FX implications than in freely floating regimes.

Findings from the selected journals

It concludes that the behavior of exchange rates and interest rates cannot be explained purely by a parity condition. While uncovered interest rate parity indicates that high-interest-rate currencies should depreciate to eliminate arbitrage opportunities, the chosen studies highlight the strong influence of time-varying risk premia as well as market expectations, investor behavior, and policy responses on exchange rates. So, interest rate differentials should be regarded with caution as leading indicators of future currency moves.

An important contribution is that long-horizon revaluations of exchange rates are related to yield-curve factors. Yung’s work finds that risk premia in the level, slope, and curvature of the yield curve explain currency returns. Interest rates matter not just for expected returns—but because they contain information regarding market expectations of risk pricing.

An additional finding reveals that exchange rate asymmetry and crash probability are also linked with interest rate differentials. Hambuckers and Ulm provide supportive grounds for the seemingly appealing high-dividend currencies but show that the broader interest rate differentials featured drive a greater magnitude of imminent collapse. Which implies that some portion of the carry trade income could simply be a reward for incurring downside tail risk.

The report also concludes that exchange rate volatility is determined by the regime type. Ulm and Hambuckers highlight that the impact of interest rate differentials on volatility is more pronounced in times of crisis and post-crisis phases. This implies that normal-period assumptions should not be relied upon unconditionally by risk managers, since volatility and correlations can switch rapidly during periods of market stress.

The other key finding is that monetary policy, or the behavior of the central bank, dominates this relationship between interest rate and exchange rate. Klaassen and Mavromatis demonstrate that central banks sometimes alter interest rates, even if slightly, to counter pressure in the exchange market. Thus, the relationship is not only “interest rates affect exchange rates” but also “exchange rate pressure feedback affects interest rate decisions.”

The fact that the chosen journals also suggest exchange rates can stay misaligned for an extended period of time. Bresser-Pereira, Feijó, and Araújo establish that capital flows, interest differentials, terms of trade, and current-account conditions may have an impact on the exchange rate. That raises doubts about the assumption that currencies will quickly trade back to their intrinsic value.

The results imply that the optimal foreign exchange risk management is state-dependent, adaptive, and forward-looking. This is because firms and financial institutions should not implement static hedging strategies or simple interest rate forecasts alone. They should instead turn to options, forwards, stress testing, scenario analysis, policy monitoring, and yield-curve information in tandem to address both short-term volatility and long-term currency misalignment.

Conclusion

This reflection leads to the conclusion that the features of interest rates—exchange rates—are best understood as an asset-pricing and policy-interaction problem rather than a simple parity condition. Interest rate differences are important factors, mostly by setting risk premia, volatility,and tail risk and interacting with the reaction functions of central banks. One obvious application of international risk management is that hedging and risk measurement should be state-dependent as the volatility and crash risk are determined by state, rather than expected depreciation alone. I have argued that in today’s world of global finance, using yield-curve knowledge, to fund your inducements for policy versus an active rates policy or the option-based hedge under high differential or stress offers a far more robust currency risk solution.

Funding

The author declares that no financial support was received for the research, authorship, and/or publication of this article.

Conflict of interest

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

1. Hambuckers J, Ulm M. On the role of interest rate differentials in the dynamic asymmetry of exchange rates. Econ Model. (2023) 129:106554. doi: 10.1016/j.econmod.2023.106554

2. Yung J. Can interest rate factors explain exchange rate fluctuations? J Empir Finance. (2021) 61:34–56. doi: 10.1016/j.jempfin.2021.01.005

3. Ulm M, Hambuckers J. Do interest rate differentials drive the volatility of exchange rates? Evidence from an extended stochastic volatility model. J Empir Finance. (2022) 65:125–48. doi: 10.1016/j.jempfin.2021.12.004

4. Klaassen F, Mavromatis K. Exchange market pressure in interest rate rules. J Int Financ Markets Inst Money. (2024) 93:102005. doi: 10.1016/j.intfin.2024.102005

5. Bresser-Pereira LC, Feijó C, Araújo EC. The determination of the exchange rate: a new-developmental approach. Struct Change Econ Dyn. (2025) 72:245–55. doi: 10.1016/j.strueco.2024.08.015

6. Ramadugu R, Doddipatla L, Yerram R. Risk management in foreign exchange for cross-border payments: strategies for minimizing exposure. Turk Online J Qual Inq. (2020) 11(2):892–900. doi: 10.53555/tojqi.v11i2.10578

© The Author(s). 2026 Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.